Autotransfusion Systems Market Size 2026-2030

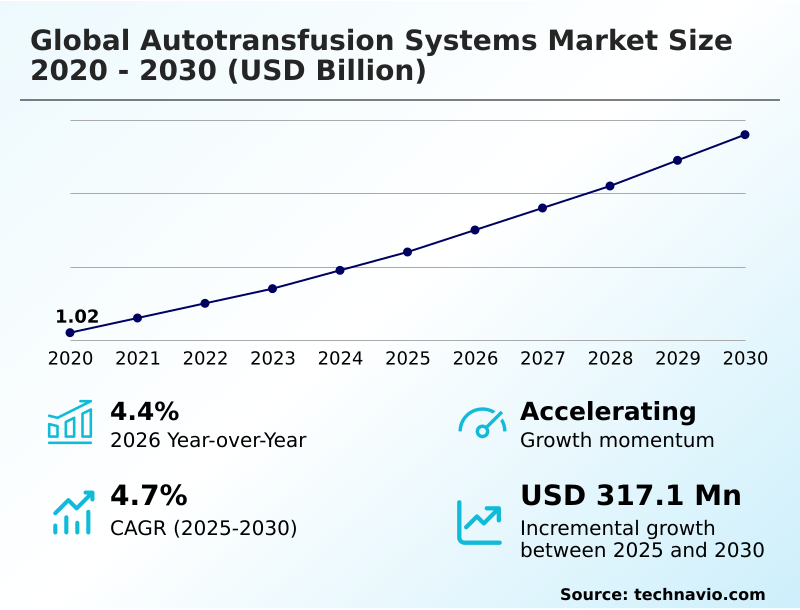

The autotransfusion systems market size is valued to increase by USD 317.1 million, at a CAGR of 4.7% from 2025 to 2030. Increasing volume of surgical procedures and growing geriatric population will drive the autotransfusion systems market.

Major Market Trends & Insights

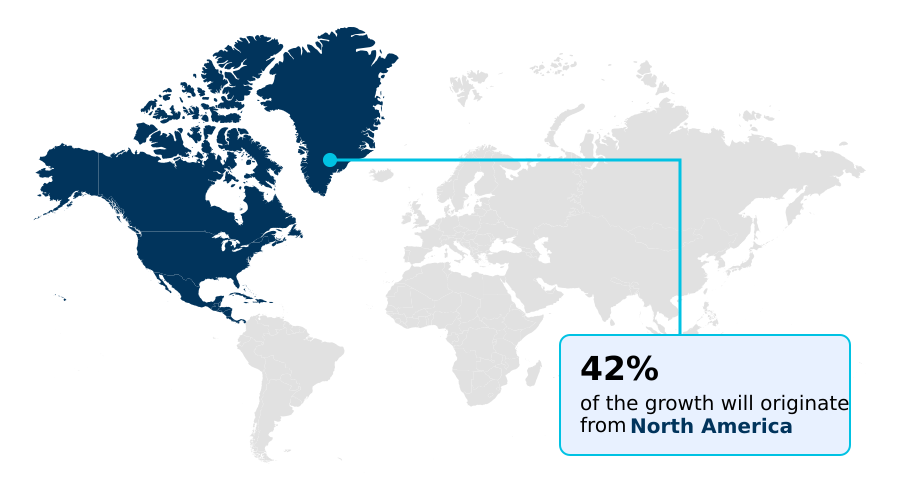

- North America dominated the market and accounted for a 42.5% growth during the forecast period.

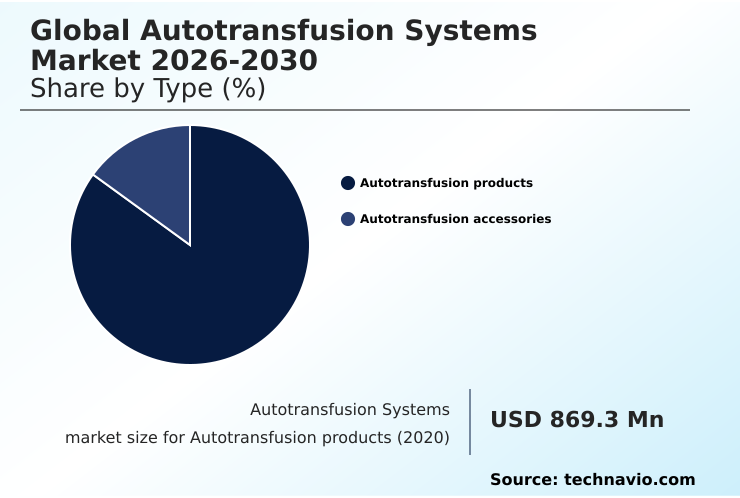

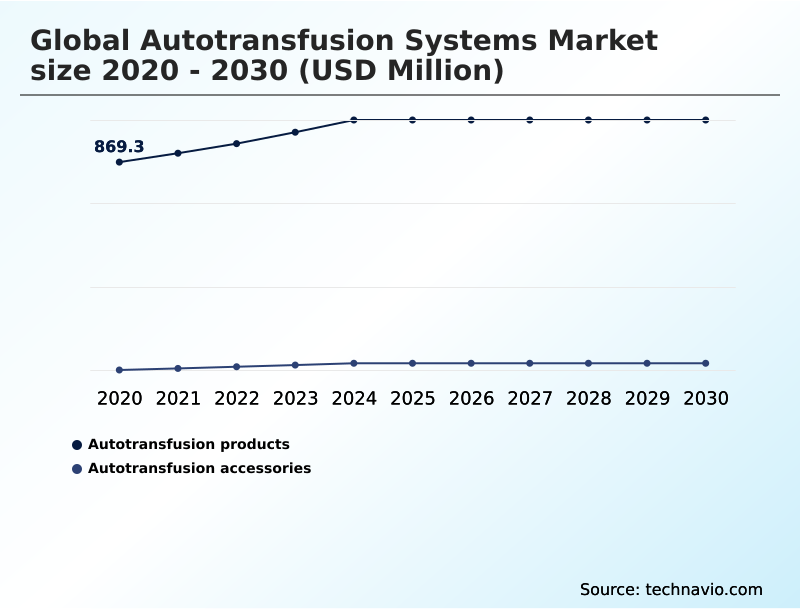

- By Type - Autotransfusion products segment was valued at USD 1.01 billion in 2024

- By End-user - Hospitals segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 537.1 million

- Market Future Opportunities: USD 317.1 million

- CAGR from 2025 to 2030 : 4.7%

Market Summary

- The autotransfusion systems market is defined by a strong clinical imperative to enhance patient safety and manage healthcare resources effectively. Growth is propelled by the rising volume of complex surgeries and the widespread adoption of patient blood management programs aimed at minimizing reliance on allogeneic blood transfusions.

- These systems, which facilitate intraoperative cell salvage, are critical in specialties like cardiac, orthopedic, and trauma surgery. Technological innovation is a key competitive differentiator, with manufacturers focusing on improving centrifugation efficiency, biocompatibility of disposables, and automation to simplify surgical workflow integration.

- For instance, a hospital system evaluating this technology might analyze how integrating a system with superior leukocyte depletion can reduce transfusion-related complications, leading to shorter hospital stays and lower overall care costs. This ROI calculation is balanced against the challenge of high capital investment and the recurring cost of single-use disposables.

- The market is also seeing an expansion into new clinical areas, such as low-blood-loss procedures and obstetrics, further broadening its application and driving deeper penetration into daily surgical practice worldwide, reinforcing the importance of robust blood conservation techniques.

What will be the Size of the Autotransfusion Systems Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Autotransfusion Systems Market Segmented?

The autotransfusion systems industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Type

- Autotransfusion products

- Autotransfusion accessories

- End-user

- Hospitals

- Clinics

- Product type

- Consumables

- Devices

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- France

- UK

- Asia

- Rest of World (ROW)

- North America

By Type Insights

The autotransfusion products segment is estimated to witness significant growth during the forecast period.

The market is segmented by offerings, including core autotransfusion products and essential accessories. The products segment, comprising cell saver systems, represents the capital investment portion of the market.

Growth is driven by the increasing frequency of complex surgeries and a heightened focus on patient blood management principles. These systems are pivotal in procedures with significant blood loss, such as cardiovascular and orthopedic operations.

Innovation is centered on improving erythrocyte recovery and the efficiency of cell washing. For example, advancements in automated cell processing have demonstrated a 15% improvement in red cell viability.

This focus on technological enhancement, like better contaminant removal and leukocyte depletion, solidifies the segment's role in advancing perioperative care standards and supporting blood conservation techniques.

The Autotransfusion products segment was valued at USD 1.01 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 42.5% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Autotransfusion Systems Market Demand is Rising in North America Request Free Sample

The geographic landscape of the autotransfusion systems market is led by North America, which holds a dominant share of over 42% due to its high volume of complex surgeries and advanced healthcare infrastructure.

This region's maturity is supported by strong patient blood management programs and favorable reimbursement, fostering deep market penetration and continuous innovation in cell salvage technology. Europe follows, with robust adoption in countries like Germany and the UK.

The Asia Pacific region, however, presents the most significant growth opportunity, driven by expanding healthcare access and increasing surgical volumes.

While facing challenges related to cost and awareness, the focus on reducing transfusion-related infections and improving perioperative care standards is accelerating the adoption of blood product alternatives.

This is leading to a greater use of surgical blood reinfusion techniques and hemofiltration.

Market Dynamics

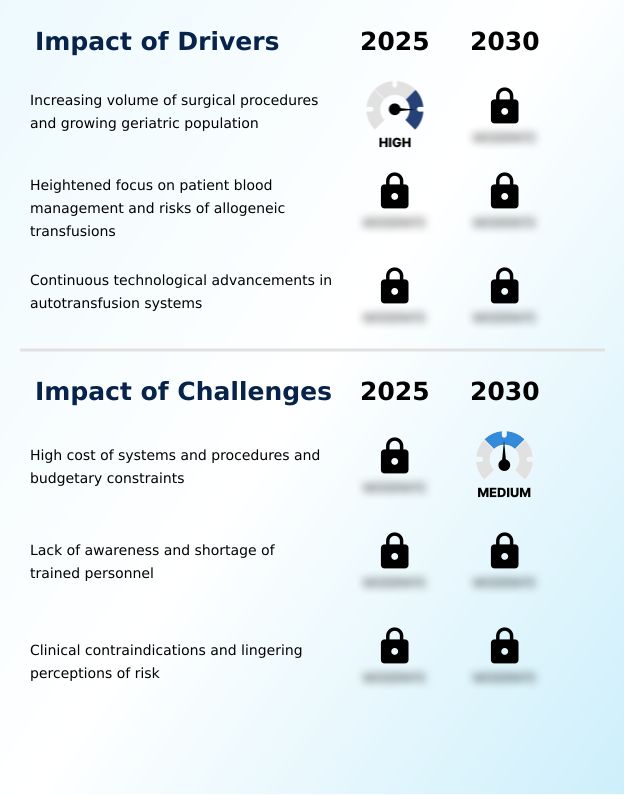

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Healthcare institutions undertaking a strategic review of their surgical services are increasingly focused on patient blood management protocols. A key consideration is the economic impact of autotransfusion programs, balancing the initial investment against long-term savings. The cost of autotransfusion disposable kits is a significant factor in this analysis, especially when evaluating its use in both high-risk and low-blood-loss procedures.

- For example, in spinal fusion surgery, the benefits of intraoperative cell salvage are well-established. When comparing autotransfusion versus allogeneic transfusion, the discussion often centers on the pronounced risks of allogeneic blood transfusion, which can lead to complications that are over 50% more costly to manage than the price of a single disposable kit.

- This makes the use of autotransfusion systems for trauma surgery a clear clinical and financial decision. The quality control in autotransfusion is paramount, with a focus on leukocyte depletion filter efficiency to mitigate inflammatory responses. As applications expand, even the role of autotransfusion use in oncology and transplant surgery is being re-evaluated.

- Proper training for autotransfusion system operators ensures adherence to protocols and addresses any contraindications for autotransfusion use, maximizing the benefits of this technology in diverse settings like orthopedic surgery and pediatric autotransfusion system design.

What are the key market drivers leading to the rise in the adoption of Autotransfusion Systems Industry?

- The increasing volume of surgical procedures worldwide, coupled with a growing geriatric population requiring more interventions, serves as a primary driver for the market.

- The market is fundamentally driven by the rising volume of surgical procedures, particularly high-blood-loss surgeries in an aging population.

- With cardiovascular surgery applications and major orthopedic procedures increasing by over 5% annually in many developed nations, the demand for effective blood conservation is intensifying.

- For the geriatric demographic, which now accounts for over 40% of complex surgical cases, minimizing the risks tied to allogeneic transfusions is a clinical imperative.

- Autotransfusion provides a critical solution, offering a safer alternative that supports better outcomes in trauma patient management and oncological resection support.

- This demographic and procedural growth creates a sustained demand for systems that facilitate reliable postoperative blood salvage and surgical blood reinfusion, making it a cornerstone of modern surgical practice and transplant surgery blood conservation.

What are the market trends shaping the Autotransfusion Systems Industry?

- A key market trend involves the expansion of clinical applications for autotransfusion systems beyond high-blood-loss procedures. This includes their strategic adoption in surgeries with low to moderate anticipated blood loss.

- A significant trend shaping the market is the expansion of autotransfusion into surgeries with lower anticipated blood loss, driven by a proactive approach to blood conservation. Historically reserved for high-risk cases, cell salvage device use is now growing in routine procedures.

- This shift is enabled by systems designed for smaller volumes, where advanced centrifugation can efficiently process salvaged blood, increasing yield by up to 20% compared to older models. This makes autologous transfusion viable for outpatient orthopedic surgeries, where avoiding even a single unit of donor blood can prevent costly transfusion-associated complications.

- This trend, promoting bloodless surgery techniques, aligns with the goals of pediatric cell salvage and obstetrics hemorrhage management, significantly broadening the technology's application and market potential with better perioperative anemia correction.

What challenges does the Autotransfusion Systems Industry face during its growth?

- The high capital cost of autotransfusion systems and associated procedural expenses, combined with hospital budgetary constraints, presents a significant challenge to market growth.

- A primary market challenge is the significant financial barrier posed by the high cost of equipment and single-use disposables. For many hospitals, the capital outlay for a new autotransfusion system can consume up to 10% of the annual equipment budget, while recurring costs for disposable collection reservoirs and sterile processing kits impact operational spending.

- This economic pressure is compounded by inconsistent reimbursement models, which may only cover 70% of the total procedural cost, creating a financial disincentive for broader adoption.

- This reality often limits the use of shed blood processing and cardiotomy suction to only the most critical cases, hindering the technology's potential to become a universal standard of care and complicating surgical team training and cost-benefit analysis.

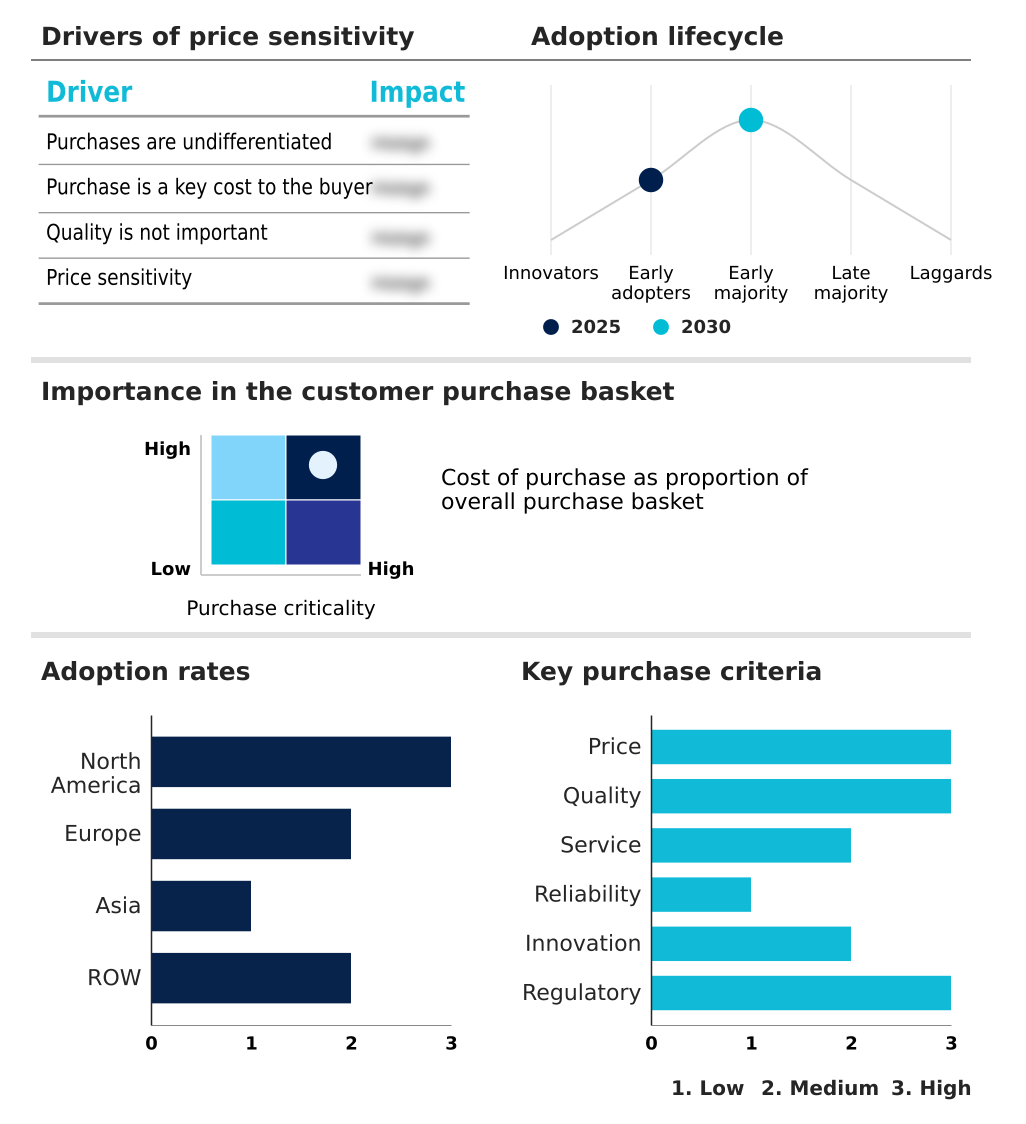

Exclusive Technavio Analysis on Customer Landscape

The autotransfusion systems market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the autotransfusion systems market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Autotransfusion Systems Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, autotransfusion systems market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Becton Dickinson and Co. - Analyzes continuous-flow devices designed for intraoperative and postoperative red blood cell separation, washing, and packing, enhancing autologous blood recovery and patient safety.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Becton Dickinson and Co.

- Beijing ZKSK Technology

- Braile Biomedica

- Fresenius Kabi AG

- Gen World Medical Devices

- Haemonetics Corp.

- i‑SEP

- LivaNova PLC

- Macopharma SA

- Medtronic Plc

- Nipro Corp.

- Redax S.p.A.

- SARSTEDT AG and Co. KG

- Stryker Corp.

- Teleflex Inc.

- Terumo Corp.

- Zimmer Biomet Holdings Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Autotransfusion systems market

- In November 2024, Fresenius Kabi AG announced a strategic partnership with a leading GPO to supply its CATSmart autotransfusion systems, aiming to expand access in mid-sized hospitals and ambulatory surgery centers.

- In January 2025, LivaNova PLC received CE Mark approval for its next-generation Xtra+ Autotransfusion System, featuring enhanced platelet recovery protocols and advanced data management for complex cardiac surgeries.

- In March 2025, UnitedHealth Group and Anthem jointly announced a new value-based care initiative rewarding ambulatory surgical centers that use intraoperative cell salvage for orthopedic surgeries, aiming to reduce post-surgical complications.

- In April 2025, Medtronic plc launched its new Auto-Intel series of autotransfusion systems, which integrate advanced sensor technology to provide real-time feedback on blood processing, maximizing red blood cell recovery.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Autotransfusion Systems Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 284 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 4.7% |

| Market growth 2026-2030 | USD 317.1 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 4.4% |

| Key countries | US, Canada, Mexico, Germany, France, UK, Italy, Spain, The Netherlands, China, Japan, India, South Korea, Indonesia, Thailand, Brazil, Saudi Arabia, UAE, Turkey, South Africa, Argentina, Colombia and Israel |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The autotransfusion systems market is evolving beyond being a niche technology for high-blood-loss surgeries into a cornerstone of modern perioperative blood management. Boardroom decisions are increasingly influenced by the dual benefits of improved patient outcomes and resource optimization.

- The adoption of systems featuring advanced cell salvage technology, such as tangential flow filtration and automated cell processing for erythrocyte recovery, is now a strategic priority. This shift is driven by a focus on mitigating the clinical and financial risks associated with allogeneic blood transfusion.

- For example, facilities using systems with superior hemolysis control and biocompatibility in their sterile disposable kits report a notable reduction in post-operative recovery times. Effective anticoagulation and plasma sequestration protocols are integral to maximizing the quality of red cell concentrate.

- The technology's value is further proven in its ability to manage blood conservation during complex procedures, from cardiotomy suction in cardiac cases to surgical site aspiration in orthopedics. Innovations in microaggregate filtration and reinfusion line filters are enhancing the safety profile, making autologous blood recovery a more reliable standard of care for packed red blood cells.

What are the Key Data Covered in this Autotransfusion Systems Market Research and Growth Report?

-

What is the expected growth of the Autotransfusion Systems Market between 2026 and 2030?

-

USD 317.1 million, at a CAGR of 4.7%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Autotransfusion products, and Autotransfusion accessories), End-user (Hospitals, and Clinics), Product Type (Consumables, and Devices) and Geography (North America, Europe, Asia, Rest of World (ROW))

-

-

Which regions are analyzed in the report?

-

North America, Europe, Asia and Rest of World (ROW)

-

-

What are the key growth drivers and market challenges?

-

Increasing volume of surgical procedures and growing geriatric population, High cost of systems and procedures and budgetary constraints

-

-

Who are the major players in the Autotransfusion Systems Market?

-

Becton Dickinson and Co., Beijing ZKSK Technology, Braile Biomedica, Fresenius Kabi AG, Gen World Medical Devices, Haemonetics Corp., i‑SEP, LivaNova PLC, Macopharma SA, Medtronic Plc, Nipro Corp., Redax S.p.A., SARSTEDT AG and Co. KG, Stryker Corp., Teleflex Inc., Terumo Corp. and Zimmer Biomet Holdings Inc.

-

Market Research Insights

- The market's dynamics are shaped by a strong focus on clinical outcomes and operational efficiency through advanced perioperative blood management. The shift toward value-based care initiatives is a significant factor, with some hospital networks reporting a 25% reduction in allogeneic transfusions after implementing comprehensive blood management programs.

- The adoption of cell salvage technology is central to this trend, as it directly mitigates the risks of transfusion-associated complications. Advanced systems featuring continuous autotransfusion capabilities offer up to a 15% improvement in processing speed, enhancing surgical workflow integration and operating room throughput.

- This efficiency, combined with the clear benefits of autologous transfusion, strengthens the cost-benefit analysis for healthcare providers, driving broader adoption despite initial capital costs and ongoing expenses for single-use disposables.

We can help! Our analysts can customize this autotransfusion systems market research report to meet your requirements.