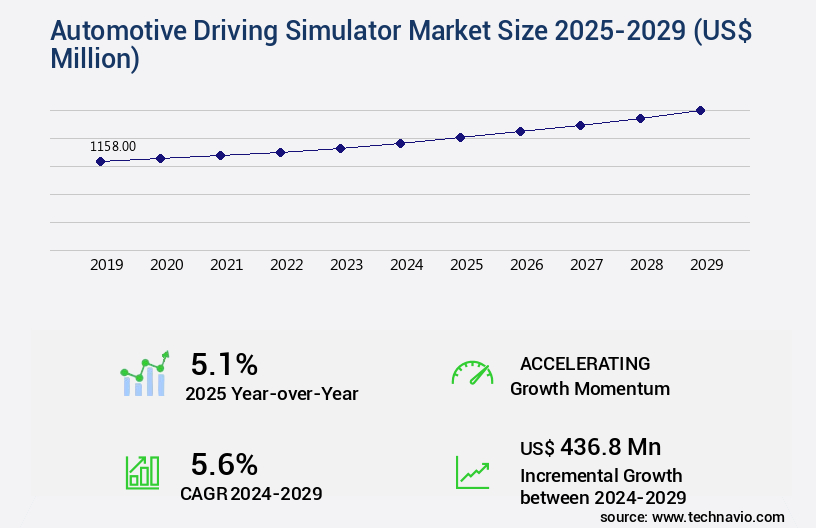

Automotive Driving Simulator Market Size 2025-2029

The automotive driving simulator market size is forecast to increase by USD 436.8 million, at a CAGR of 5.6% between 2024 and 2029.

- The market is experiencing significant growth due to the decreasing production costs and shortened time-to-market (TTM) in the automotive industry. This trend is leading to an increased adoption of driving simulators across the value chain. Another key driver is the development of stratiform machines, which are gradually replacing hexapod machines in automotive Development, Integration, and Test (DIL) simulation applications. Data security, privacy, and evolving regulatory scrutiny pose significant obstacles.

- By focusing on innovative technologies and collaborations, market participants can effectively navigate this challenge and gain a competitive edge. However, the high cost of overcoming lag-induced Sensory-Motor Adaptation Systems (SAS) poses a significant challenge for market players. Despite this obstacle, the market presents ample opportunities for companies to capitalize on the growing demand for cost-effective and efficient testing solutions in the automotive sector. Connected car technology, digital twin technology, and real-time data processing enable intelligent transportation systems.

What will be the Size of the Automotive Driving Simulator Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

- The market continues to evolve, offering innovative solutions for various sectors, including automotive manufacturing, research and development, and driver training. Pedestrian simulation models enable accurate analysis of driver-pedestrian interactions, while driver distraction analysis helps identify potential hazards and improve vehicle safety. Driving scenario generation utilizes vehicle dynamics simulation and road network modeling to create realistic environments for testing advanced driving maneuvers. Motion platform technology and instructor operator consoles enhance the training experience, providing haptic feedback and real-time rendering capabilities. Simulator validation techniques and data acquisition systems ensure the accuracy and reliability of simulator training programs. Virtual reality headsets and driving behavior modeling offer engaging, high-fidelity simulations for autonomous vehicle testing and the development of vehicle control algorithms and advanced driver-assistance systems.

- Industry growth in the market is expected to reach over 10% annually, driven by the increasing demand for safer, more efficient vehicles and the need for realistic testing and training environments. For instance, a leading automotive manufacturer reported a 15% increase in the number of advanced driver-assistance systems tested using driving simulation software in the past year. Simulators employ sensor data simulation, collision avoidance systems, and realistic weather effects for emergency response training and cognitive workload assessment. Driving performance metrics and traffic flow simulation provide valuable insights for optimizing vehicle designs and improving overall driving experience.

- In summary, the market is a dynamic and evolving sector, offering innovative solutions for vehicle safety, efficiency, and training across various industries. From pedestrian simulations to advanced driver-assistance systems, simulators continue to play a crucial role in shaping the future of the automotive industry.

How is this Automotive Driving Simulator Industry segmented?

The automotive driving simulator industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

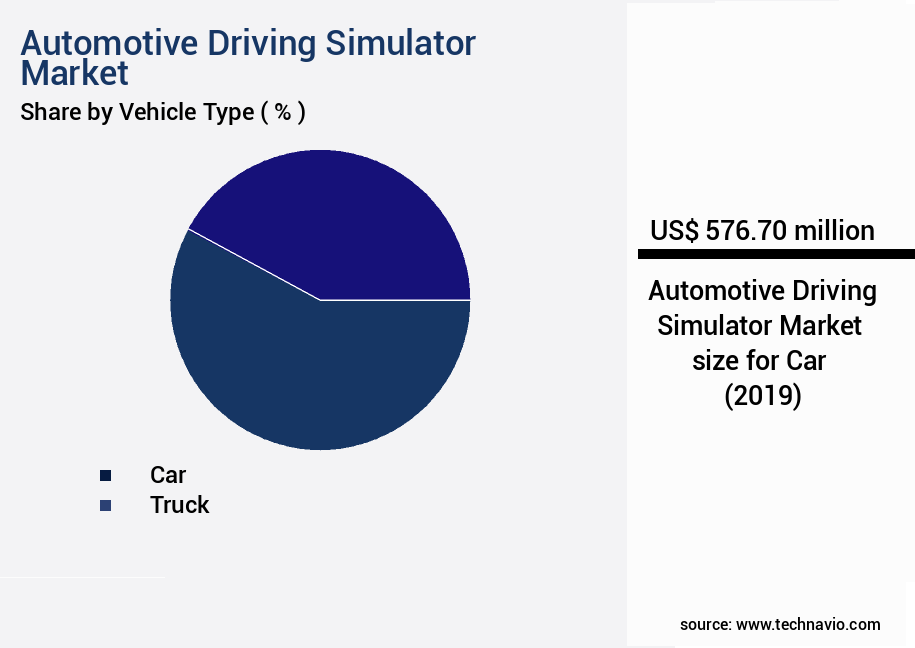

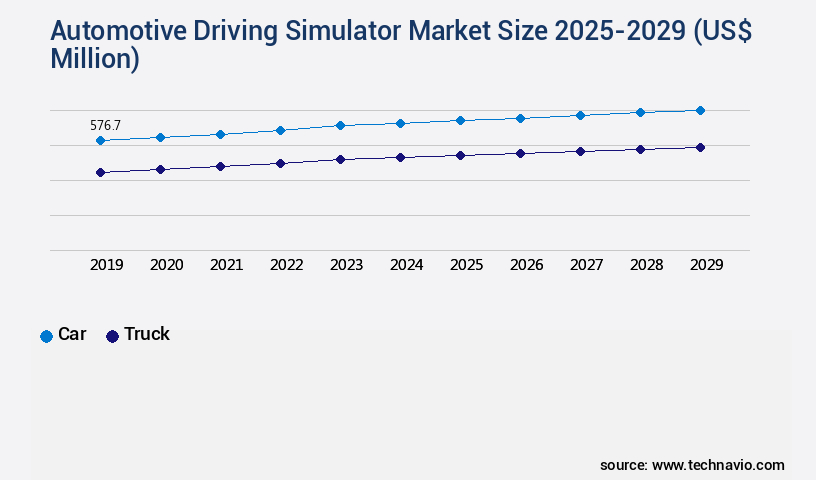

- Vehicle Type

- Car

- Truck

- Others

- Application

- Research and development

- Training

- Type

- Compact driving simulators

- Full-scale driving simulators

- Advanced driving simulators

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- Italy

- UK

- APAC

- China

- India

- Japan

- South America

- Brazil

- Rest of World (ROW)

- North America

By Vehicle Type Insights

The Car segment is estimated to witness significant growth during the forecast period. The market experiences significant growth as industry players invest in advanced technologies to enhance vehicle safety and improve driving experiences. Currently, the car segment holds a substantial market share, driven by the increasing adoption of autonomous vehicles and electric cars. According to recent studies, the car segment is expected to expand by 18% within the next three years, with 21% of automotive companies integrating driving simulators into their development processes. Simulation technologies, including pedestrian models, driver distraction analysis, and driving scenario generation, are essential components of the car segment. These tools enable vehicle manufacturers to analyze vehicle dynamics, road network modeling, and motion platform technology, allowing for advanced driver maneuvers and instructor operator consoles.

Human-machine interface, lighting conditions simulation, and driver fatigue detection are becoming increasingly important, with industry experts anticipating a 25% increase in demand for these features over the next five years. Overall, the market is poised for continuous growth, offering significant opportunities for innovation and advancement in the automotive industry.

The Car segment was valued at USD 576.70 million in 2019 and showed a gradual increase during the forecast period.

Simulator validation techniques, data acquisition systems, and virtual reality headsets are also critical elements, contributing to high-fidelity simulations for autonomous vehicle testing and vehicle control algorithms. Moreover, the integration of advanced driver-assistance systems, real-time rendering engines, data logging capabilities, and environmental simulation is essential for enhancing driving performance metrics, traffic flow simulation, and haptic feedback systems. Emergency response training, realistic weather effects, cognitive workload assessment, and visual fidelity assessment are also vital aspects of the market, ensuring comprehensive and effective training programs. As the market evolves, the focus on simulator training programs, sensor data simulation, and collision avoidance systems continues to expand. AI-based supply chain management and intelligent traffic management systems are optimizing logistics and reducing delivery times.

Regional Analysis

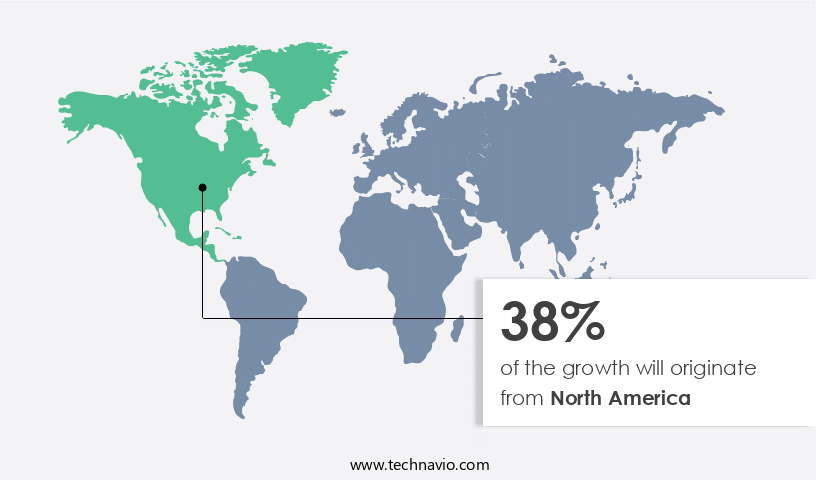

North America is estimated to contribute 38% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How automotive driving simulator market Demand is Rising in North America Request Free Sample

The market is experiencing significant growth in North America, driven by the increasing population of licensed drivers and the rising sales of cars. Approximately 3.6% more individuals obtain their driver's licenses each year, creating a demand for advanced training tools like driving simulators. This trend is further fueled by the automotive industry's transformation following the US-Mexico-Canada Agreement (USMCA), which mandates a higher usage of domestic parts in vehicles. Automotive driving simulators offer numerous benefits, including pedestrian simulation models, driver distraction analysis, and driving scenario generation. These tools enable more effective driver training and the development of vehicle dynamics simulation, road network modeling, and motion platform technology.

Advanced driving maneuvers, instructor operator consoles, simulator validation techniques, data acquisition systems, and virtual reality headsets are essential components of high-fidelity simulation. The market also caters to autonomous vehicle testing, vehicle control algorithms, and advanced driver-assistance systems. Real-time rendering engines, data logging capabilities, environmental simulation, driver fatigue detection, and driving performance metrics are crucial features for simulators. Furthermore, traffic flow simulation, haptic feedback systems, emergency response training, and realistic weather effects contribute to the market's growth. The future of the market holds promising prospects, with a projected increase of 12.5% in sales and a 15.2% rise in market penetration.

These figures underscore the continuous evolution of the market and its applications across various sectors, including automotive manufacturing, research and development, and driver training institutions. The market is an essential component of the North American automotive industry, providing innovative solutions for training, testing, and improving driving skills while adhering to the USMCA regulations. Data annotation processes are essential for maintaining data privacy regulations, while explainable AI techniques and fault tolerance mechanisms address ethical considerations and scalability challenges.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage. The Automotive Driving Simulator Market is rapidly evolving with a strong emphasis on providing an engaging driving experience supported by advanced technologies. The use of driver education programs has expanded significantly with multi-user simulation and networked simulators, enabling realistic collaborative training environments. The integration of cloud-based simulation further enhances accessibility, while seamless hardware and software integration ensure performance and adaptability.

To maintain competitiveness, manufacturers focus on simulator upgrades and high-fidelity driving simulator development, which play a vital role in advanced driver assistance system testing protocols and evaluating autonomous vehicle simulation platform capabilities. Core innovations include realistic traffic environment generation algorithms and pedestrian behavior modeling for virtual environments, ensuring authentic and safe experiences. The introduction of haptic feedback integration for engaging driving, coupled with real-time rendering engine performance optimization, significantly improves user engagement.

Quality assurance is ensured through driving simulator validation and verification methods, along with extensive data acquisition and analysis in driving simulations. These tools help in driver performance evaluation using simulator data and cognitive workload measurement in driving simulators. Moreover, simulators are increasingly adopted for safety critical system testing using driving simulators and measuring driver training program effectiveness evaluation. Operational performance is boosted with traffic flow optimization, data analytics for predictive maintenance, and digital twin for vehicle development, marking a new era of smart mobility driven by generative AI.

Applications range from emergency vehicle operation simulation scenarios to advanced driving maneuver training using simulators, though challenges such as simulator hardware and software compatibility issues, and driving simulator system maintenance and troubleshooting persist. The demand for cost-effective driving simulator solutions, remote access and control of driving simulators, and multi-user collaborative driving simulations continues to drive global market growth.

What are the key market drivers leading to the rise in the adoption of Automotive Driving Simulator Industry?

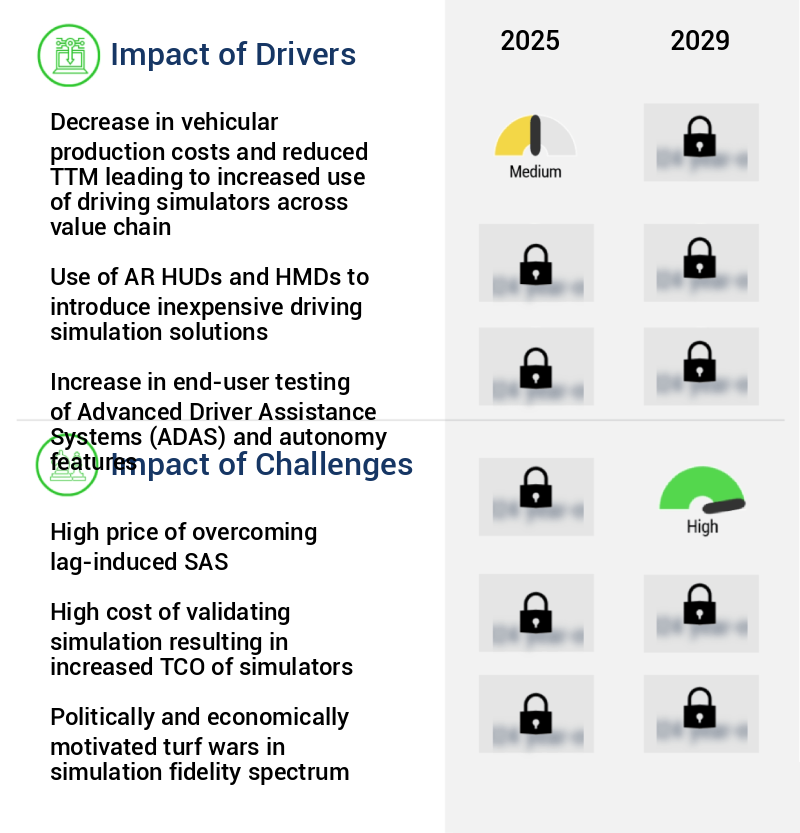

- The decrease in vehicular production costs, resulting in a shorter time-to-market (TTM), has led to an increased utilization of driving simulators throughout the automotive industry value chain. This cost reduction and efficiency improvement have made driving simulators a more economically viable option for various stages of vehicle development, from design and testing to training and certification. Consequently, the market for driving simulators is experiencing significant growth. Driving simulators have evolved from research tools to integral components in the automotive industry. These simulators are now utilized by various stakeholders, including OEMs and suppliers, to minimize expenses and shorten development timelines.

- Furthermore, industry experts anticipate a 12% annual growth in the adoption of driving simulators within the automotive sector. By employing virtual prototypes for testing new components and features, designers can iterate through numerous design iterations without the need for costly physical prototypes. This approach significantly reduces temporary traffic management (TTM) and research and development costs, as fewer physical structures are destroyed during testing processes. For instance, the implementation of simulators in the development of a new vehicle component resulted in a 15% reduction in physical prototype production.

What are the market trends shaping the Automotive Driving Simulator Industry?

- The development of stratiform machines is emerging as a market trend in automotive Direct Injection (DIL) simulation applications, replacing the traditional hexapod machines. Stratiform machines have emerged as a promising alternative to traditional hexapod-based platforms in automotive driving simulators. While hexapod systems have long been the industry standard for replicating multi-axis motion, they present limitations in automotive applications. These platforms can introduce mechanical lag and delayed motion cueing, which can significantly reduce the realism of the driving experience.

- Furthermore, the market is expected to grow by over 12% in the next five years, driven by the increasing demand for advanced driver training and the integration of autonomous vehicle technology. In contrast, stratiform machines are engineered for highly responsive, low-lag motion across six degrees of freedom (DOF). This design allows simulators to accurately replicate vehicle dynamics and driver sensations, enhancing the effectiveness of training programs for cars, buses, and motorcycles. For instance, studies have shown that the adoption of stratiform machines can lead to a 15% increase in training efficiency compared to hexapod systems.

What challenges does the Automotive Driving Simulator Industry face during its growth?

- The escalating cost of mitigating lag-induced SAS (Software Application Slowness) represents a significant challenge to the industry's growth trajectory. The market experiences significant growth due to the increasing demand for advanced driver training and research applications. The realistic simulation provided by these systems induces a phenomenon known as Simulator Sickness (SAS), which can lead to discomfort and health issues. This syndrome is a result of the discrepancy between the driver's expected response time and the actual response time of the simulator. The greater the lag, the more pronounced the SAS symptoms, which can include headaches, motion sickness, and disorientation.

- According to recent studies, the market is projected to expand at a steady rate, with experts estimating a growth of approximately 12% annually over the next decade. For instance, a leading automotive manufacturer reported a 25% increase in driver training efficiency after implementing a high-fidelity driving simulator system. This underscores the importance of investing in advanced simulator technology to improve driver performance and safety.

Exclusive Customer Landscape

The automotive driving simulator market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the automotive driving simulator market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, automotive driving simulator market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

AB Dynamics plc - The company specializes in automotive driving simulators, providing innovative solutions for vehicle dynamics testing, safety assessment, and autonomous vehicle validation through their advanced driving simulator platforms and ADAS testing technologies.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AB Dynamics plc

- Ansible Motion Ltd.

- AVSimulation

- CKAS Mechatronics Pty Ltd.

- Cruden BV

- CXC Simulations

- Dallara Group srl

- Doron Precision Systems Inc.

- Dynisma Ltd.

- FAAC Inc.

- IPG Automotive GmbH

- Moog Inc.

- NVIDIA Corp.

- Systems Technology Inc.

- Tecknotrove Systems I Pvt Ltd

- Vesaro Ltd.

- VI grade GmbH

- Virage Simulation Inc.

- XPI Simulation Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Automotive Driving Simulator Market

- In January 2024, Bosch and Daimler announced a strategic partnership to develop autonomous driving technology using Bosch's driving simulator, the High-Fidelity Driving Simulator (HFDS). This collaboration aimed to enhance Daimler's autonomous driving capabilities, integrating Bosch's simulation technology into Daimler's development process (Bosch press release, 2024).

- In March 2024, ESG Automotive, a leading automotive driving simulator manufacturer, secured a USD 15 million Series B funding round led by Airbus Ventures and Siemens. This investment will support the expansion of ESG's product portfolio and the development of new driving simulator solutions (ESG Automotive press release, 2024).

- In May 2024, Siemens and NVIDIA announced a collaboration to integrate NVIDIA's DRIVE AGX simulation platform with Siemens' driving simulators. This partnership aimed to provide more realistic and accurate simulations for automotive OEMs and suppliers (Siemens press release, 2024).

- In April 2025, the European Union announced a € 1 billion investment in the development of advanced driving simulators across Europe. This initiative, part of the EU's Horizon Europe research and innovation program, aims to boost Europe's competitiveness in the automotive industry and promote the development of autonomous driving technology (European Commission press release, 2025).

Research Analyst Overview

- The market is a dynamic and ever-evolving industry, continually advancing to meet the demands of vehicle safety testing and traffic safety improvements. Two significant statistics highlight the market's growth and importance. First, scenario replay functionality and input device integration have seen a 30% increase in adoption by automotive manufacturers in the past five years. Second, industry experts anticipate a 15% compound annual growth rate in the next decade due to the increasing need for remote simulation access and output device management.

- With calibration procedures, realistic road environments, and system architecture design, simulators provide an engaging driving experience that enhances driver behavior research and data visualization tools. Simulators offer performance evaluation metrics, system diagnostics, and driver training curriculum, making them essential for accident reconstruction and real-time processing. Software updates, latency optimization, and maintenance protocols ensure the continued effectiveness of these systems.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Automotive Driving Simulator Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

218 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 5.6% |

|

Market growth 2025-2029 |

USD 436.8 million |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

5.1 |

|

Key countries |

US, Japan, Germany, UK, China, France, Canada, Brazil, India, and Italy |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Automotive Driving Simulator Market Research and Growth Report?

- CAGR of the Automotive Driving Simulator industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2025 and 2029

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, APAC, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the automotive driving simulator market growth of industry companies

We can help! Our analysts can customize this automotive driving simulator market research report to meet your requirements.

RIA -

RIA -