Automotive Clutch Market Size 2024-2028

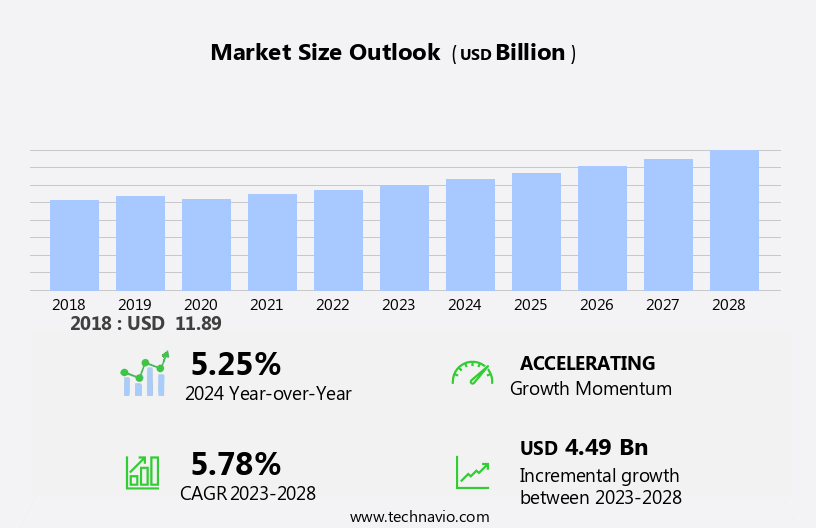

The automotive clutch market size is forecast to increase by USD 4.49 billion at a CAGR of 5.78% between 2023 and 2028. The market is experiencing significant growth due to several key factors. Rising disposable incomes and a shift in consumer preferences towards advanced vehicles are driving the demand for sophisticated transmission systems, such as Fully Automatic Transmissions (FATs), Automated Manual Transmissions (AMTs), and Dual-Clutch Transmissions (DCTs). These advanced transmissions are increasingly popular due to their smooth shifting and improved fuel efficiency. Moreover, governments around the world are offering subsidies to encourage the adoption of eco-friendly vehicles, further boosting the market growth. However, the market is not without challenges. Regulatory bodies are imposing stringent requirements on clutch systems to ensure durability and reliability, which increases the manufacturing costs. Standard-bearer companies, such as Tesla, are setting new benchmarks for vehicle performance and efficiency, putting pressure on other players to innovate and differentiate. The market analysis report provides a comprehensive study of these trends and challenges, offering valuable insights for stakeholders in the automotive industry.

What will be the Size of the Market During the Forecast Period?

The market is a vital component of manual vehicle transmission systems, enabling the smooth transfer of rotational power from the engine shaft to the transmission systems. This market caters to both manual transmission vehicles and emerging automatic transmission technologies. Manual clutches have long been the cornerstone of manual transmission vehicles, facilitating the connection and disconnection of the engine and transmission during gear changes. However, the increasing focus of Original Equipment Manufacturers (OEMs) on producing automatic transmission systems, such as torque converters, has led to a shift in market dynamics.

Moreover, consumer preference plays a significant role in the market. While manual transmission vehicles offer a more engaging driving experience, automatic transmission systems provide convenience and ease of use. The global operations of automotive hubs in various regions, including emerging economies, are expanding, contributing to the growth of the market. Production capacity is a crucial factor influencing the market. OEMs are investing in advanced production facilities to increase their output and meet the growing demand for both manual and automatic transmission vehicles. The fossil fuel dependency of the automotive industry poses a challenge to the market, as the shift towards electric vehicles gains momentum.

The torque converter, a key component of automatic transmission systems, has gained popularity due to its ability to provide a seamless driving experience. However, the manual clutch continues to hold its ground in the market, particularly in passenger cars, where cost and fuel efficiency remain essential considerations. The market is characterized by a global presence, with major players operating in various regions. The industry is driven by technological advancements, increasing demand for efficient transmission systems, and the growing popularity of electric vehicles. In conclusion, the market is a dynamic and evolving industry, influenced by various factors such as consumer preference, production capacity, and technological advancements.

In conclusion, the shift towards automatic transmission systems and the growing popularity of electric vehicles present both opportunities and challenges for market participants. OEMs must adapt to these trends while maintaining their focus on delivering high-quality, efficient, and cost-effective clutch solutions to meet the diverse needs of the global automotive market.

Market Segmentation

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Channel

- OEM

- Aftermarket

- Vehicle Type

- Passenger vehicles

- Commercial vehicles

- Geography

- APAC

- China

- Japan

- North America

- US

- Europe

- UK

- France

- South America

- Middle East and Africa

- APAC

By Channel Insights

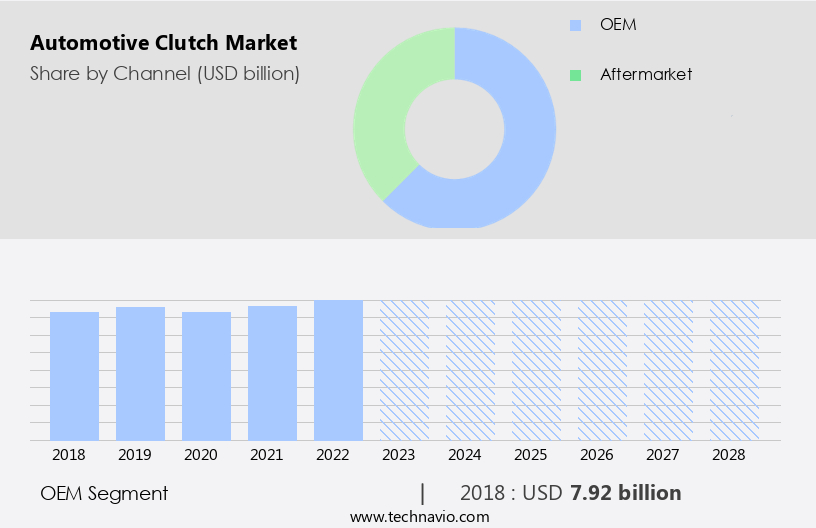

The OEM segment is estimated to witness significant growth during the forecast period. In the market, Original Equipment Manufacturers (OEMs) distribute their clutch products through various channels to reach customers worldwide. OEMs primarily sell automotive clutches to vehicle manufacturers for installation during production, accounting for a substantial portion of OEM clutch sales. This direct sales channel is crucial for automakers, as they require dependable clutch systems to ensure vehicle performance and durability. Furthermore, OEMs may partner with authorized dealerships and distributors to supply clutch components for aftermarket services and repairs. These authorized channels offer customers authentic OEM parts, safeguarding their vehicles' integrity and warranties.

Get a glance at the market share of various segments Request Free Sample

The OEM segment was valued at USD 7.92 billion in 2018 and showed a gradual increase during the forecast period.

Regional Insights

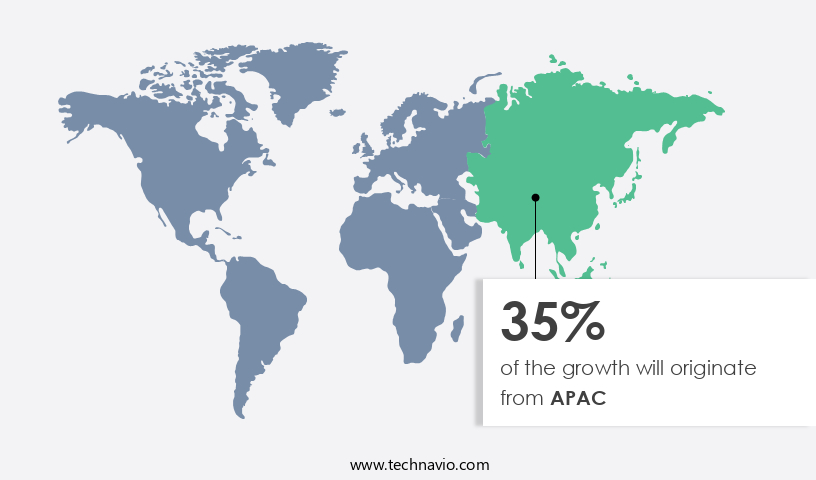

APAC is estimated to contribute 35% to the growth of the global market during the forecast period. Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions Request Free Sample

The Asia-Pacific (APAC) region plays a pivotal role in The market due to its expanding automotive industry, population growth, and escalating demand for passenger and commercial vehicles. Notable countries like China, Japan, India, and South Korea significantly impact the APAC market, given their thriving automotive sectors and increasing vehicle production. China, the world's largest automotive market, fuels substantial demand for automotive clutches, primarily due to its advanced manufacturing sector and burgeoning vehicle manufacturing industry.

Moreover, Japan and South Korea, recognized for their innovative automotive technologies, house leading automakers such as Toyota, Honda, and Hyundai, who incorporate premium clutches into their vehicles to ensure optimal performance. The APAC region is expected to dominate the global EV market, with China being the largest market shareholder. This trend is expected to create a significant demand for automotive clutches in the region. In summary, the APAC region, driven by countries like China, Japan, and South Korea, holds immense potential for the market due to its expanding automotive industry, population growth, and increasing demand for passenger and commercial vehicles, including electric vehicles.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

Market Driver

Rising disposable incomes and changing consumer preferences toward advanced vehicles is the key driver of the market. The market is experiencing significant growth due to increasing consumer preferences for advanced manual and automatic transmission systems in manual vehicles. These transmission systems offer benefits such as improved rotational power transfer from the engine shaft to the transmission systems, smoother gear shifts, and enhanced driving comfort. The market is witnessing a shift towards electric vehicles (EVs) and semiautomatic transmissions, including fully automatic and torque convertor systems. OEMs are focusing on expanding their production capacity and global operations to cater to this growing demand. Government subsidies and incentives for EVs in emerging economies are further fueling the market's growth.

Consumers' increasing focus on advanced features and technologies, including connectivity and autonomous driving, is driving the demand for sophisticated clutch solutions. The market is expected to continue its growth trajectory as the automotive industry evolves towards electrification and advanced transmission technologies.

Market Trends

Increasing demand for automated manual transmissions (AMTs) and dual-clutch transmissions (DCTs) is the upcoming trend in the market. The market is experiencing significant growth due to the increasing consumer preference for advanced transmission systems in manual vehicles. Automotive clutch solutions, such as automated manual transmissions (AMTs) and dual-clutch transmissions (DCTs), offer improved rotational power transfer from the engine shaft to the transmission systems. These advanced transmissions provide smoother gear shifts, enhanced driving comfort, and better fuel efficiency compared to traditional manual transmissions. As the demand for vehicles with automated manual and dual-clutch transmissions continues to rise, key Original Equipment Manufacturers (OEMs) are focusing on expanding their production capacity to meet consumer needs. BorgWarner Inc., a leading player in The market, is one such company that caters to this trend by providing advanced transmission solutions, including clutches, for a wide range of vehicles, including passenger cars and commercial vehicles.

Moreover, the increasing popularity of electric vehicles (EVs) and the ongoing expansion of automotive hubs in emerging economies are also contributing to the growth of the market. Government subsidies and incentives for the adoption of electric vehicles and the establishment of new production facilities further bolster market growth. In summary, the market is driven by the increasing demand for advanced transmission technologies in manual vehicles, the expansion of production capacity by OEMs, and the growing popularity of electric vehicles. BorgWarner Inc. Is one of the prominent players in this market, offering innovative transmission solutions for various vehicle types.

Market Challenge

Stringent regulatory requirements on clutch systems to meet durability and reliability standards is a key challenge affecting the market growth. The market faces stringent regulatory requirements to ensure clutch systems meet durability and reliability standards set by governments worldwide. In the EU, clutch systems must comply with European Commission directives on vehicle safety and emissions, undergoing rigorous testing to demonstrate compliance. Similarly, in the US, the National Highway Traffic Safety Administration (NHTSA) sets safety standards through Federal Motor Vehicle Safety Standards (FMVSS). These regulations aim to enhance vehicle safety, performance, and longevity by mandating high-quality clutch systems. Manual transmission vehicles, such as passenger cars and commercial vehicles, primarily utilize manual clutches. However, the increasing focus on automatic transmission systems, including fully automatic and semiautomatic transmissions, may impact the manual clutch market.

However, OEMs (Original Equipment Manufacturers) are expanding their production capacity to meet the growing demand for automatic transmissions, with some, like Tesla, focusing solely on electric vehicles and their proprietary torque convertor systems. The automotive hubs in emerging economies, such as China and India, are witnessing significant growth due to increasing consumer preference for affordable vehicles. This trend may influence the market, as manual transmission vehicles are often more cost-effective than their automatic counterparts. Additionally, government subsidies in these regions may further boost the demand for manual transmission vehicles and, consequently, the manual clutch market.

In summary, The market is subject to regulatory requirements ensuring clutch systems meet durability and reliability standards. The increasing focus on automatic transmissions and the growth of emerging economies may impact the market dynamics. OEMs are expanding their production capacity to cater to the demand for automatic transmissions, while consumer preference and government subsidies in emerging economies may favor manual transmission vehicles.

Exclusive Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

AISIN CORP.: The company offers automotive clutches such as the NVR (Noise Vibration Reduction) Clutch system that has been adopted into the automotive industry as Original Equipment.

The market research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AISIN CORP.

- BorgWarner Inc.

- Burg Germany GmbH

- Eaton Corp. Plc

- EXEDY Corp.

- FCC Clutch India Pvt. Ltd.

- GMP Friction Products

- NSK Ltd.

- Schaeffler AG

- SEPAC Inc.

- The Rowland Co.

- Valeo SA

- Wabtec Corp.

- WPT Power Corp.

- ZF Friedrichshafen AG

- Honda Motor Co. Ltd.

- Hyundai Motor Co.

- Mercedes Benz Group AG

- Nissan Motor Co. Ltd.

- Toyota Motor Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

The market plays a crucial role in manual vehicles with manual transmissions, facilitating the transfer of rotational power from the engine shaft to the transmission systems. Consumer preference for manual transmissions varies, particularly in passenger cars, with OEMs focusing on both manual and automatic transmission options.

In summary, automotive hubs, including torque convertors, are integral components of automatic transmission systems. Global operations in the market span across emerging economies, driven by increasing production capacity and government subsidies. The industry's focus on innovation extends to electric vehicles, with the development of clutches for semiautomatic and fully automatic transmissions. The market's growth is influenced by the ongoing shift towards electric and alternative fuel vehicles, as well as advancements in technology and manufacturing processes. Passenger cars remain a significant market for automotive clutches, with manual clutches continuing to be a popular choice for those seeking a more engaging driving experience. The industry's future looks promising, with ongoing research and development efforts aimed at improving efficiency, performance, and sustainability.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

163 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 5.78% |

|

Market growth 2024-2028 |

USD 4.49 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

5.25 |

|

Regional analysis |

APAC, North America, Europe, South America, and Middle East and Africa |

|

Performing market contribution |

APAC at 35% |

|

Key countries |

US, China, Japan, UK, and France |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

|

Key companies profiled |

AISIN CORP., BorgWarner Inc., Burg Germany GmbH, Eaton Corp. Plc, EXEDY Corp., FCC Clutch India Pvt. Ltd., GMP Friction Products, NSK Ltd., Schaeffler AG, SEPAC Inc., The Rowland Co., Valeo SA, Wabtec Corp., WPT Power Corp., ZF Friedrichshafen AG, Honda Motor Co. Ltd., Hyundai Motor Co., Mercedes Benz Group AG, Nissan Motor Co. Ltd., and Toyota Motor Corp. |

|

Market dynamics |

Parent market analysis, market growth inducers and obstacles, market forecast, fast-growing and slow-growing segment analysis, COVID-19 impact and recovery analysis and future consumer dynamics, market condition analysis for the forecast period |

|

Customization purview |

If our market report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

What are the Key Data Covered in this Market Research and Growth Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across APAC, North America, Europe, South America, and Middle East and Africa

- Thorough analysis of the market’s competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements. Get in touch

RIA -

RIA -