Artificial Intelligence-based Cybersecurity Market Size 2026-2030

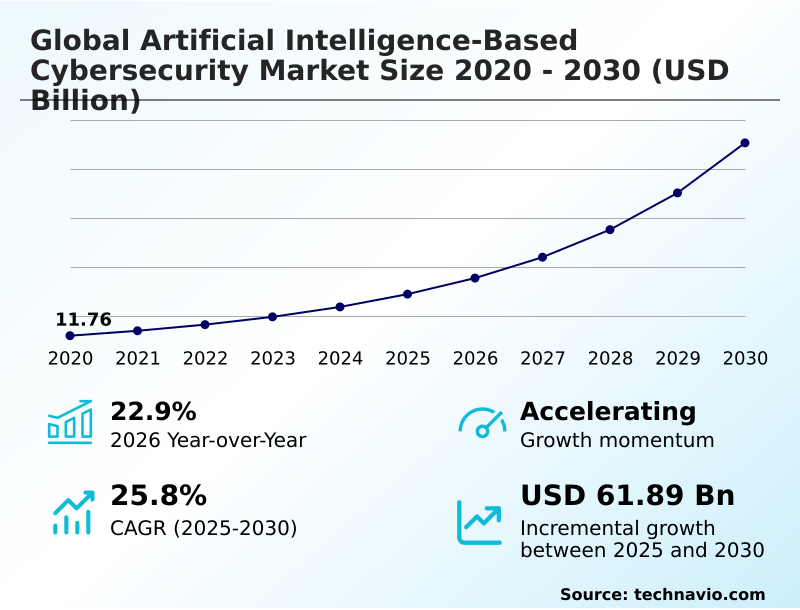

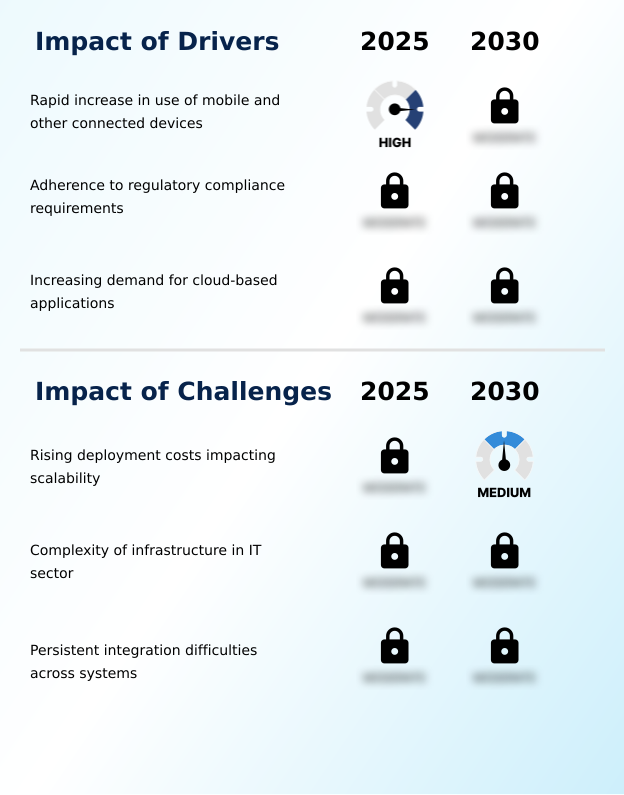

The artificial intelligence-based cybersecurity market size is valued to increase by USD 61.89 billion, at a CAGR of 25.8% from 2025 to 2030. Rapid increase in use of mobile and other connected devices will drive the artificial intelligence-based cybersecurity market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 44.2% growth during the forecast period.

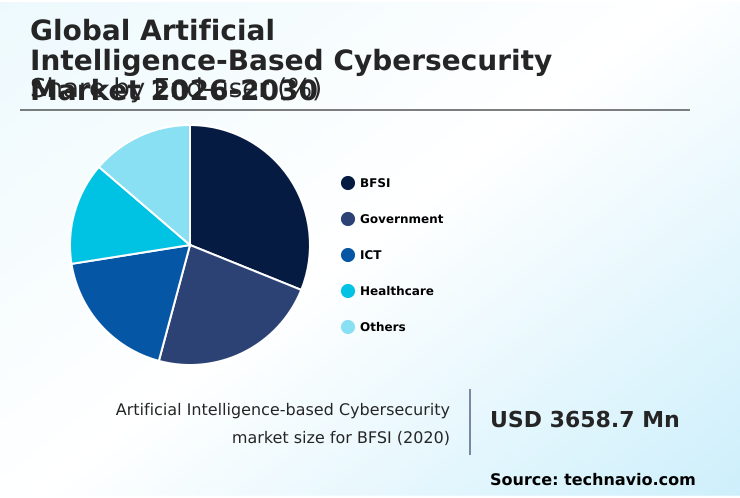

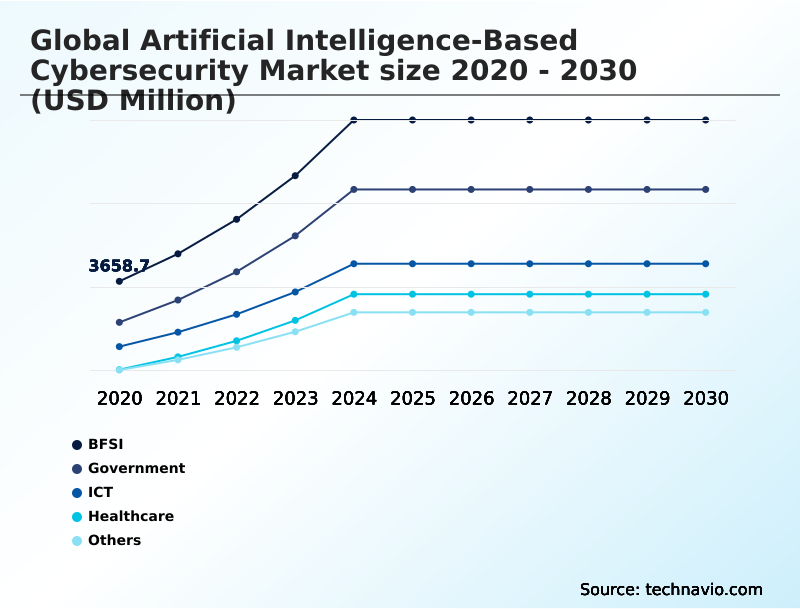

- By End-user - BFSI segment was valued at USD 7.38 billion in 2024

- By Deployment - Cloud segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 78.89 billion

- Market Future Opportunities: USD 61.89 billion

- CAGR from 2025 to 2030 : 25.8%

Market Summary

- The artificial intelligence-based cybersecurity market is defined by its application of machine learning and pattern recognition to unstructured data, uncovering novel threats that evade traditional security measures. By analyzing vast datasets, these systems learn to identify and predict evolving cyberattacks, developing expertise that mimics human intuition.

- Key drivers include the proliferation of IoT devices and the increasing demand for cloud-based applications, which create complex security environments. As a result, organizations are leveraging AI for predictive threat detection and automated response. For example, a financial institution might use behavioral analytics to instantly flag anomalous transaction patterns, preventing fraud before it impacts customers.

- This proactive stance is essential for managing sophisticated threats and adhering to stringent regulatory compliance. However, the high cost of deployment and the complexity of integrating these advanced platforms with legacy systems remain significant challenges, influencing adoption rates across various industries. This dynamic necessitates a strategic approach to security investment, balancing innovation with operational realities.

What will be the Size of the Artificial Intelligence-based Cybersecurity Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Artificial Intelligence-based Cybersecurity Market Segmented?

The artificial intelligence-based cybersecurity industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- End-user

- BFSI

- Government

- ICT

- Healthcare

- Others

- Deployment

- Cloud

- On-premises

- Component

- Software

- Services

- Hardware

- Geography

- APAC

- China

- India

- Japan

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- South America

- Brazil

- Argentina

- Colombia

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- APAC

By End-user Insights

The bfsi segment is estimated to witness significant growth during the forecast period.

The BFSI sector's adoption of artificial intelligence-based cybersecurity is driven by the necessity to protect high-value assets.

Financial institutions are migrating to cloud environments, which expands their attack surface and requires advanced defense mechanisms like behavioral analytics and ai-driven security operations.

To counter AI-automated phishing and synthetic identity fraud, the industry is shifting toward using generative AI for real-time fraud detection. This evolution is also shaped by strict regulatory mandates for cyber incident detection.

One advanced generative AI model improves fraud detection rates by an average of 20%, showcasing the power of ai for network security.

This move to autonomous cyber defense systems and real-time fraud scoring is critical, as is securing the software supply chain through robust ai governance frameworks.

The BFSI segment was valued at USD 7.38 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

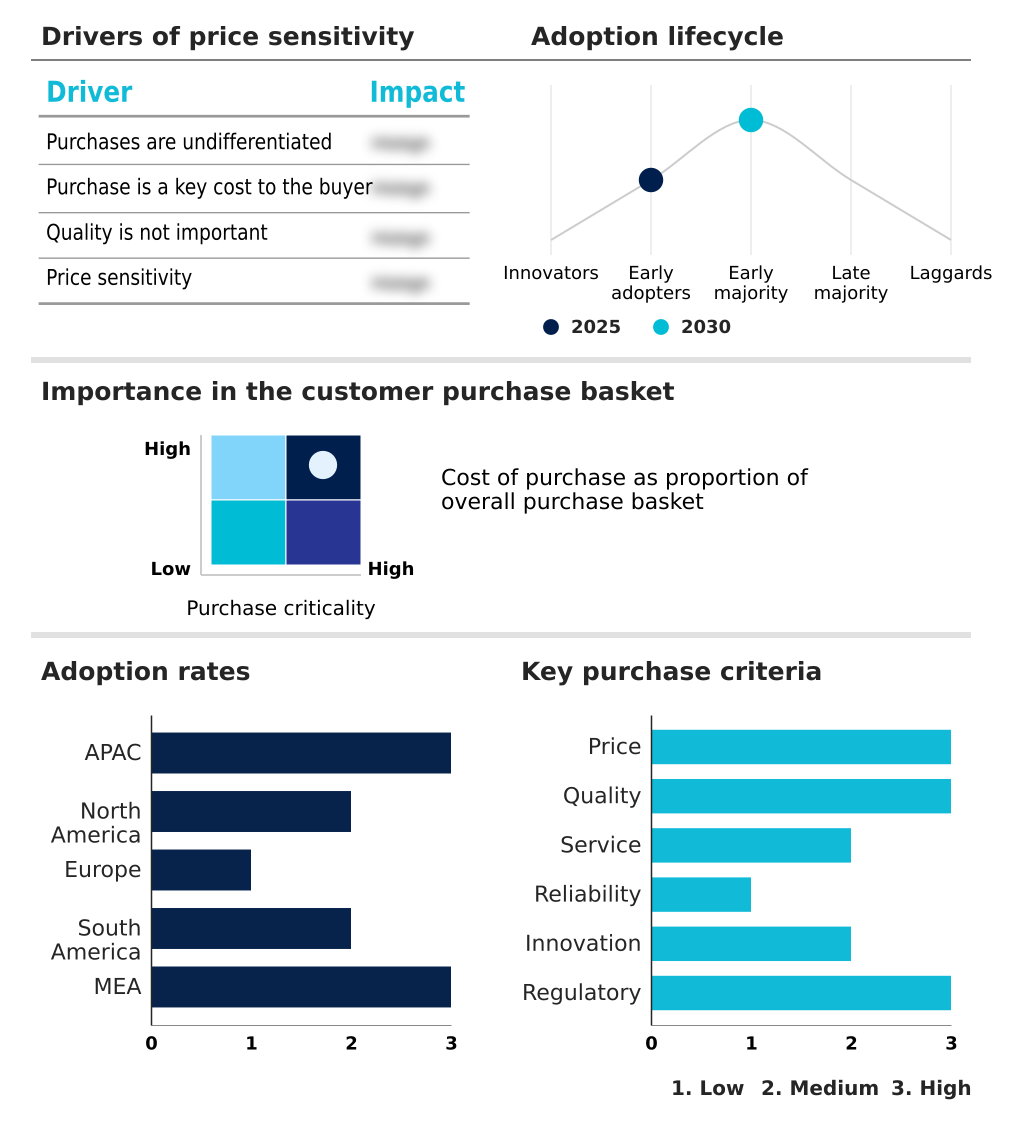

APAC is estimated to contribute 44.2% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Artificial Intelligence-based Cybersecurity Market Demand is Rising in APAC Request Free Sample

The geographic landscape of the artificial intelligence-based cybersecurity market is diverse, with North America and APAC leading in adoption and innovation.

APAC is projected to be the fastest-growing region, contributing over 44% of the market's incremental growth, driven by rapid digitization and distinct regulatory frameworks.

In North America, which accounts for over 26% of the market, a mature technological infrastructure and aggressive government initiatives foster a competitive environment focused on generative AI in threat hunting.

Europe prioritizes data sovereignty and compliance, driving demand for explainable AI and sovereign AI solutions. This regional differentiation in deploying on-premise AI cybersecurity and managing ai security risks creates a complex but opportunity-rich global market.

The focus on privacy-preserving ai and securing operational technology also varies significantly across these key regions.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The role of AI in cybersecurity has evolved from a supplementary tool to a foundational pillar of modern defense strategies. Organizations increasingly understand the benefits of AI in threat detection, particularly its ability to identify and neutralize threats in real time. The question is no longer if AI is needed, but how AI automates security response effectively.

- This has led to the development of AI driven endpoint protection platforms and cloud native AI security solutions that provide comprehensive coverage. For smaller enterprises, the concern often revolves around the cost of implementing AI cybersecurity, though hybrid models are making it more accessible.

- Key applications include using AI for preventing phishing attacks and leveraging generative AI for threat intelligence to anticipate adversary tactics. In specialized sectors, AI in financial services cybersecurity is crucial for combating sophisticated fraud, while AI based security for IoT is vital for protecting interconnected device ecosystems.

- The on-premises AI security deployment benefits, such as enhanced data control, are compelling for organizations with strict regulatory needs. A key challenge remains in securing AI models from attacks, a discipline that is rapidly advancing. Furthermore, the use of natural language processing for security and machine learning in malware detection has become standard.

- The adoption of AI for protecting critical infrastructure, where downtime is unacceptable, is nearly double that of less critical sectors, underscoring its importance in ensuring operational continuity.

What are the key market drivers leading to the rise in the adoption of Artificial Intelligence-based Cybersecurity Industry?

- The rapid increase in the use of mobile and other connected devices, which expands the potential attack surface, is a key driver for the artificial intelligence-based cybersecurity market.

- The market is primarily driven by the exponential growth of connected devices and the widespread adoption of cloud services, both of which significantly expand the digital attack surface.

- The proliferation of IoT devices necessitates advanced solutions for securing iot with ai, as many lack robust, built-in security, making real-time monitoring essential.

- Increased reliance on cloud applications for critical business functions drives the need for sophisticated cloud security with AI, capable of protecting vast amounts of sensitive data.

- Regulatory adherence is another major driver, with frameworks like GDPR and HIPAA compelling organizations to implement AI in compliance automation. This includes using natural language processing to analyze compliance documents, which can reduce audit preparation time by over 30%.

- These factors collectively fuel the demand for security for 5g networks and advanced ai-native security architecture.

What are the market trends shaping the Artificial Intelligence-based Cybersecurity Industry?

- The rising adoption of AI-powered chatbots to combat sophisticated cyberattacks is a significant emerging trend, as these systems assist analysts by automating threat detection and response.

- Key market trends are centered on the adoption of advanced AI capabilities to augment security operations. The integration of conversational AI for security and hybrid model deployment security offers operational flexibility and enhanced threat analysis.

- Businesses are leveraging AI-powered chatbots not just for customer engagement but also for real-time security alerts, with some platforms reducing analyst response time by up to 40%. This trend toward automation addresses the persistent shortage of skilled cybersecurity professionals. Furthermore, the adoption of cloud-enabled solutions continues to drive demand for AI-based security.

- The use of unsupervised algorithms helps in detecting novel threats within complex cloud environments. These advancements, including ai-driven red teaming, are shifting security from a reactive to a proactive discipline, improving resilience against sophisticated cyberattacks by an estimated 25% in certain deployments.

What challenges does the Artificial Intelligence-based Cybersecurity Industry face during its growth?

- Rising deployment costs that impact the scalability of advanced solutions present a key challenge affecting the growth of the artificial intelligence-based cybersecurity industry.

- Significant challenges persist, primarily related to cost, complexity, and integration. The high deployment cost of AI-driven cybersecurity solutions, which includes infrastructure, specialized talent, and ongoing maintenance, remains a barrier, particularly for smaller enterprises.

- The increasing complexity of IT infrastructure, intensified by the convergence of IoT, cloud, and edge computing, makes it difficult to deploy and manage security solutions like endpoint detection and response effectively. Integration with legacy systems is a persistent issue, as incompatible architectures can create security gaps and operational disruptions, sometimes increasing vulnerability exposure by 15% during transition periods.

- These challenges are compounded by a lack of standardized frameworks, forcing organizations to navigate a fragmented landscape while facing threats from prompt injection attacks and other sophisticated methods used in cyberespionage and data loss prevention.

Exclusive Technavio Analysis on Customer Landscape

The artificial intelligence-based cybersecurity market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the artificial intelligence-based cybersecurity market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Artificial Intelligence-based Cybersecurity Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, artificial intelligence-based cybersecurity market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Amazon Web Services Inc. - Key solutions include AI-based cybersecurity leveraging cloud-native platforms, delivering scalable and integrated threat protection for modern digital infrastructures and distributed workloads.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Amazon Web Services Inc.

- AO Kaspersky Lab

- BlackBerry Ltd.

- Broadcom Inc.

- Check Point Software Tech Ltd.

- Cisco Systems Inc.

- CrowdStrike Inc.

- Dell Technologies Inc.

- Fortinet Inc.

- Hewlett Packard

- IBM Corp.

- Intel Corp.

- Juniper Networks Inc.

- LogRhythm Inc.

- NVIDIA Corp.

- S.C. BITDEFENDER S.R.L.

- Securonix Inc.

- Tech Mahindra Ltd.

- Vectra AI Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Artificial intelligence-based cybersecurity market

- In August 2024, IBM Consulting launched the Cybersecurity Assistant, a generative AI tool integrated into its Threat Detection and Response (TDR) services to accelerate threat investigations.

- In October 2024, SentinelOne and Amazon Web Services expanded their strategic collaboration to leverage Amazon Bedrock for developing advanced threat analysis and response capabilities.

- In February 2025, CrowdStrike introduced Charlotte AI Detection Triage, a feature designed to autonomously validate and prioritize security alerts using agentic AI.

- In April 2025, CyberArk launched identity-centric secure AI agents, signaling a market evolution from passive AI assistance to autonomous defense mechanisms for identity security.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Artificial Intelligence-based Cybersecurity Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 302 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 25.8% |

| Market growth 2026-2030 | USD 61888.5 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 22.9% |

| Key countries | China, India, Japan, South Korea, Australia, Indonesia, US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, Brazil, Argentina, Colombia, Saudi Arabia, UAE, South Africa, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The artificial intelligence-based cybersecurity market has matured, moving beyond simple machine learning to embrace advanced autonomous defense systems. Core technologies like generative AI and large language models are now central to product development, enabling predictive threat detection and real-time remediation. This shift toward AI-native security platforms allows for sophisticated anomaly detection and automated response to zero-day exploits.

- In boardrooms, this technological evolution directly impacts budgeting, as investment pivots from legacy tools to agentic AI and secure AI agents that can automate security operations center tasks. Organizations now prioritize solutions offering effective network segmentation and deep threat intelligence.

- This strategic focus is validated by performance metrics; for instance, some integrated AI systems have demonstrated a 30% reduction in threat investigation time. The adoption of specialized hardware, such as neural processing units and data processing units, further accelerates these capabilities, making AI security posture management a critical priority for enterprises aiming to counter advanced cyberespionage and adversarial attacks.

What are the Key Data Covered in this Artificial Intelligence-based Cybersecurity Market Research and Growth Report?

-

What is the expected growth of the Artificial Intelligence-based Cybersecurity Market between 2026 and 2030?

-

USD 61.89 billion, at a CAGR of 25.8%

-

-

What segmentation does the market report cover?

-

The report is segmented by End-user (BFSI, Government, ICT, Healthcare, and Others), Deployment (Cloud, and On-premises), Component (Software, Services, and Hardware) and Geography (APAC, North America, Europe, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Rapid increase in use of mobile and other connected devices, Rising deployment costs impacting scalability

-

-

Who are the major players in the Artificial Intelligence-based Cybersecurity Market?

-

Amazon Web Services Inc., AO Kaspersky Lab, BlackBerry Ltd., Broadcom Inc., Check Point Software Tech Ltd., Cisco Systems Inc., CrowdStrike Inc., Dell Technologies Inc., Fortinet Inc., Hewlett Packard, IBM Corp., Intel Corp., Juniper Networks Inc., LogRhythm Inc., NVIDIA Corp., S.C. BITDEFENDER S.R.L., Securonix Inc., Tech Mahindra Ltd. and Vectra AI Inc.

-

Market Research Insights

- The artificial intelligence-based cybersecurity market is characterized by a rapid shift toward automated and predictive defense mechanisms. Adoption is accelerating as organizations achieve measurable outcomes, with some improving fraud detection accuracy by over 20% and reducing incident response times by more than half. The use of threat detection using machine learning is becoming standard for managing high-volume alerts.

- Predictive analytics for cyber threats enables a proactive posture, a stark contrast to the reactive models of the past. As threat actors leverage AI, deploying autonomous cyber defense systems is no longer optional.

- This dynamic compels businesses to invest in solutions that offer not only superior detection but also tangible ROI through enhanced operational efficiency and risk mitigation, validating the strategic importance of AI in modern security frameworks.

We can help! Our analysts can customize this artificial intelligence-based cybersecurity market research report to meet your requirements.