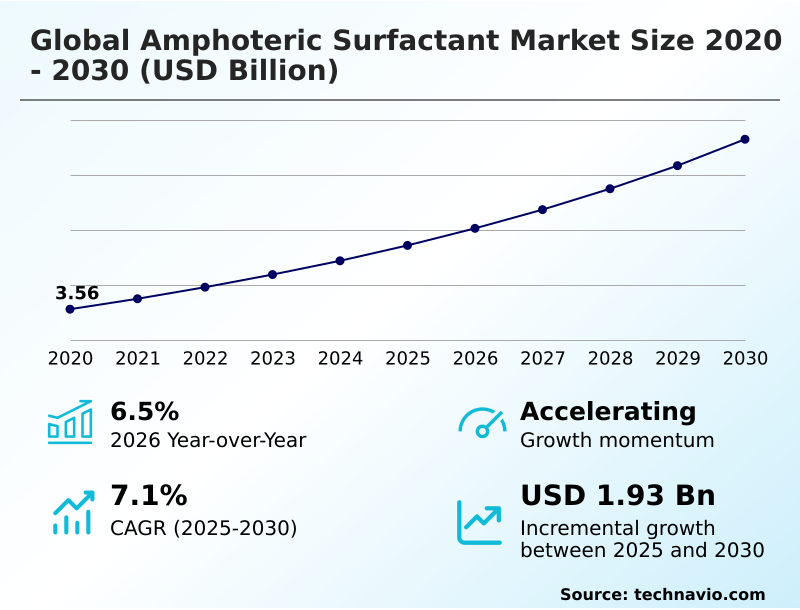

Amphoteric Surfactant Market Size 2026-2030

The amphoteric surfactant market size is valued to increase by USD 1.93 billion, at a CAGR of 7.1% from 2025 to 2030. Escalating demand for mild and sulfate-free personal care formulations will drive the amphoteric surfactant market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 43% growth during the forecast period.

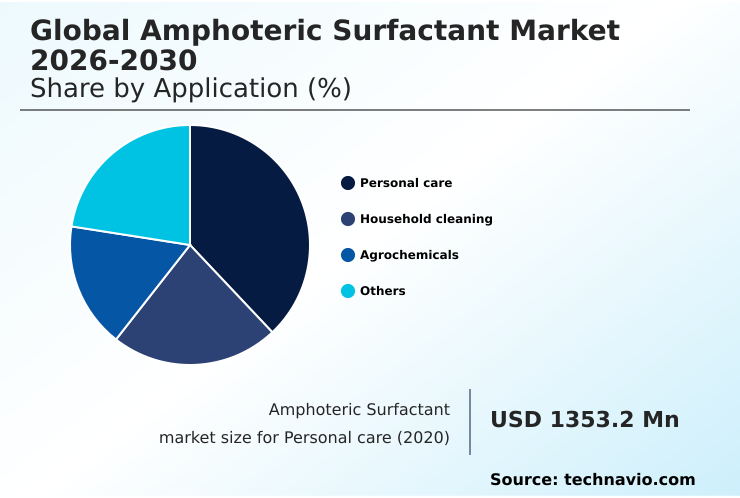

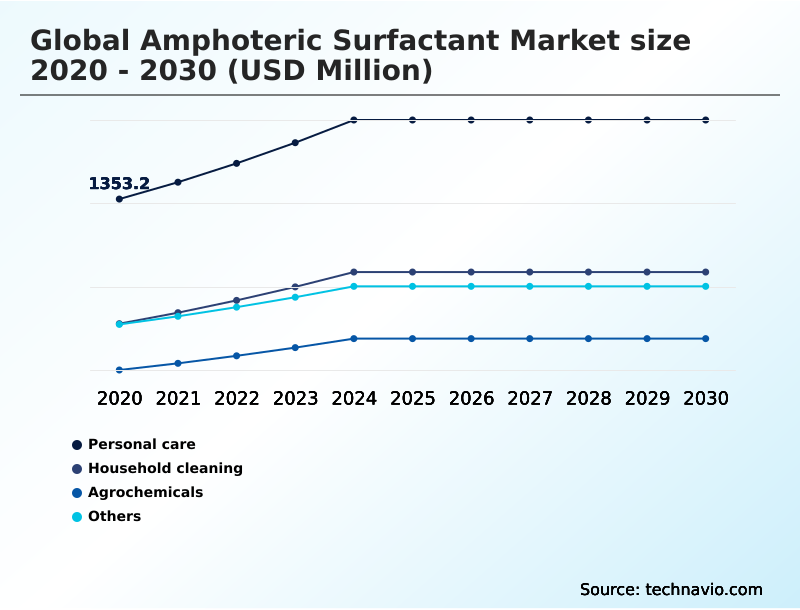

- By Application - Personal care segment was valued at USD 1.70 billion in 2024

- By Type - Betaines segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 3.09 billion

- Market Future Opportunities: USD 1.93 billion

- CAGR from 2025 to 2030 : 7.1%

Market Summary

- The amphoteric surfactant market is defined by its versatile zwitterionic surfactant chemistry, which is crucial for creating high-performance, non-irritating formulations. Growth is driven by the escalating demand for sulfate-free cleansing systems in personal care and the need for stable, multifunctional agents in industrial applications.

- A significant trend involves the strategic shift from petrochemical derivatives to sustainable oleochemical feedstocks to improve the environmental footprint of products. However, this pivot introduces challenges related to raw material price volatility and supply chain complexities.

- For instance, a formulator of industrial cleaners must balance the cost-performance ratio of bio-based ingredients against conventional options, a decision that directly impacts production budgets and market positioning. This dynamic requires manufacturers to innovate continuously, developing high-purity amphoterics and leveraging green chemistry principles to meet both regulatory mandates and evolving consumer expectations for safety and sustainability.

What will be the Size of the Amphoteric Surfactant Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Amphoteric Surfactant Market Segmented?

The amphoteric surfactant industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Application

- Personal care

- Household cleaning

- Agrochemicals

- Others

- Type

- Betaines

- Aminoxides

- Others

- End-user

- Cosmetics

- Food and beverage

- Others

- Geography

- APAC

- China

- Japan

- India

- Europe

- Germany

- UK

- France

- North America

- US

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Colombia

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- APAC

By Application Insights

The personal care segment is estimated to witness significant growth during the forecast period.

The personal care segment is a dominant force, driven by the clean beauty movement and demand for skin-friendly cleansers. Formulators prioritize zwitterionic surfactant chemistry for mild surfactant systems in premium hair care ingredients and sensitive skin products.

The use of oleochemical feedstocks is central to creating high-purity amphoterics. Innovations in cocamidopropyl betaine synthesis and the development of sultaine derivatives and amine oxide surfactants are enabling low-salt surfactant systems suitable for baby care formulations.

This focus on gentle yet effective ingredients is critical, as the segment accounts for a substantial portion of market innovation, with development cycles often being 25% faster than in industrial segments to meet rapidly changing consumer preferences.

The Personal care segment was valued at USD 1.70 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

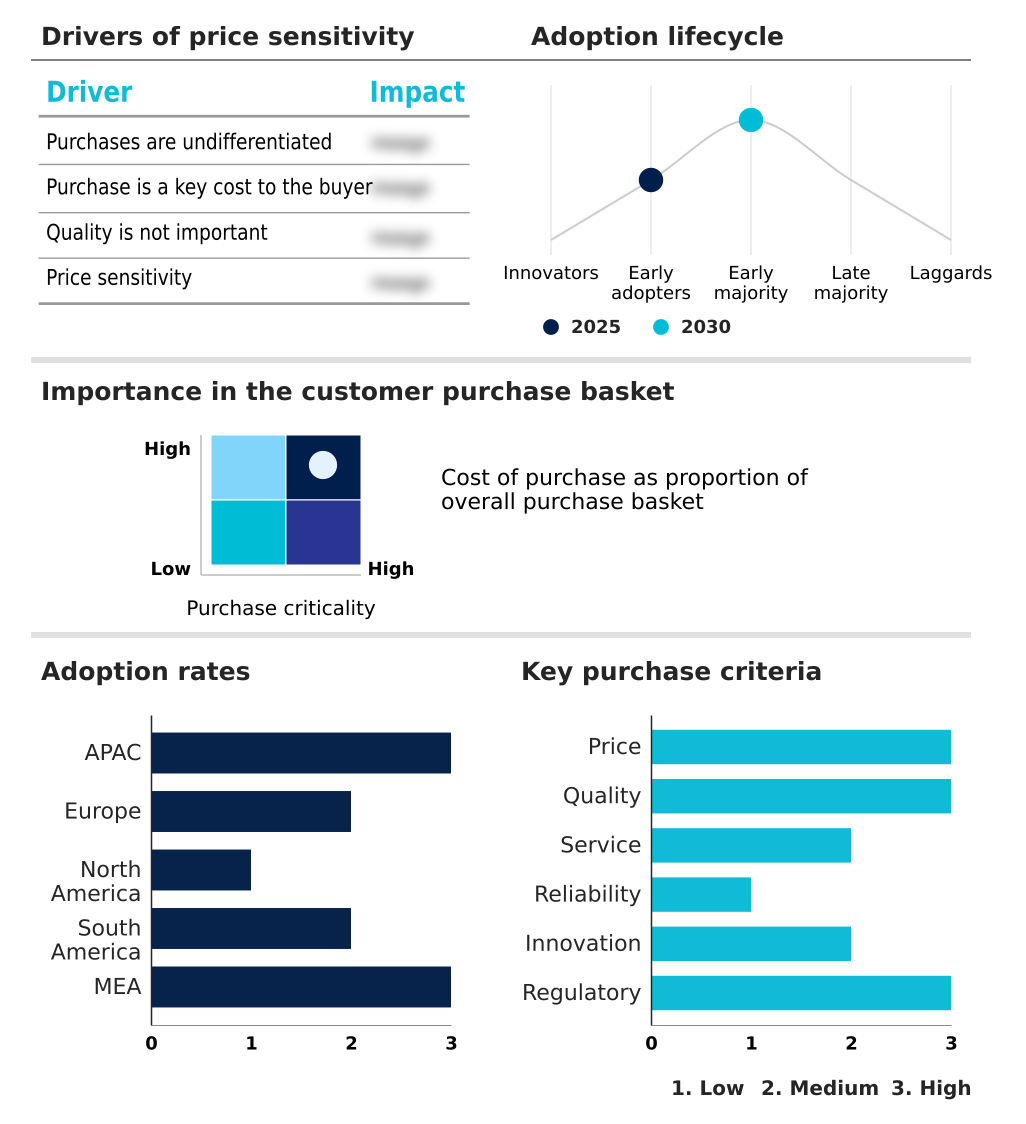

APAC is estimated to contribute 43% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Amphoteric Surfactant Market Demand is Rising in APAC Request Free Sample

The geographic landscape is characterized by diverse regional demands and production capabilities. APAC is the primary growth engine, projected to contribute 43% of the market's incremental growth, with a regional CAGR of 7.5%, outpacing North America's 6.6%.

This expansion is driven by rising demand for high-value cosmetic grades and institutional cleaning solutions.

European markets are heavily influenced by stringent regulations like EU Ecolabel compliance, which require detailed REACH registration data and aquatic toxicity assessment, promoting the use of concentrated detergent systems and high-active formulations.

North America focuses on dermo-cosmetic compatibility and anti-static finishing agents. In this environment, manufacturers are adopting mass balance certification to verify their renewable carbon index, while navigating commodity chemical pricing for feedstocks to remain competitive in developing rinse-free cleansing agents.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Formulators are continually seeking the best amphoteric surfactant for sulfate-free shampoo, often comparing cocamidopropyl betaine vs cocamidopropyl hydroxysultaine for performance benefits. The demand for mild amphoteric surfactants for baby wash is particularly strong, driving innovation in high-foaming amphoteric surfactants for cleansers that remain gentle. Beyond personal care, amphoteric surfactant use in agricultural adjuvants is expanding to improve crop protection efficacy.

- Similarly, their unique properties are leveraged in amphoteric surfactants for high-salinity oilfields. The push for sustainability has increased the search for biodegradable amphoteric surfactants for green cleaners and natural alternatives to cocamidopropyl betaine. Understanding amphoteric surfactant compatibility with anionic surfactants is crucial for reducing irritation potential with amphoteric surfactants. This synergy also aids in viscosity building with low-salt amphoteric surfactants.

- In industrial applications, amine oxide surfactants in bleach-based cleaners provide stability, while amphoteric hydrotropes in concentrated detergents enable high-active formulations. The role of amphoteric surfactants in micellar water highlights their mild cleansing power.

- The industrial sector uses them for specialized tasks such as amphoteric surfactants for industrial metal cleaning, leveraging their temperature stability of amphoteric drilling fluids, and in amphoteric surfactants in textile scouring processes.

- The cost analysis of oleochemical vs petrochemical surfactants remains a key consideration, with companies managing regulatory challenges for amphoteric surfactant impurities to ensure market access for products like food-contact safe amphoteric emulsifiers, which show 15% better stability in certain systems.

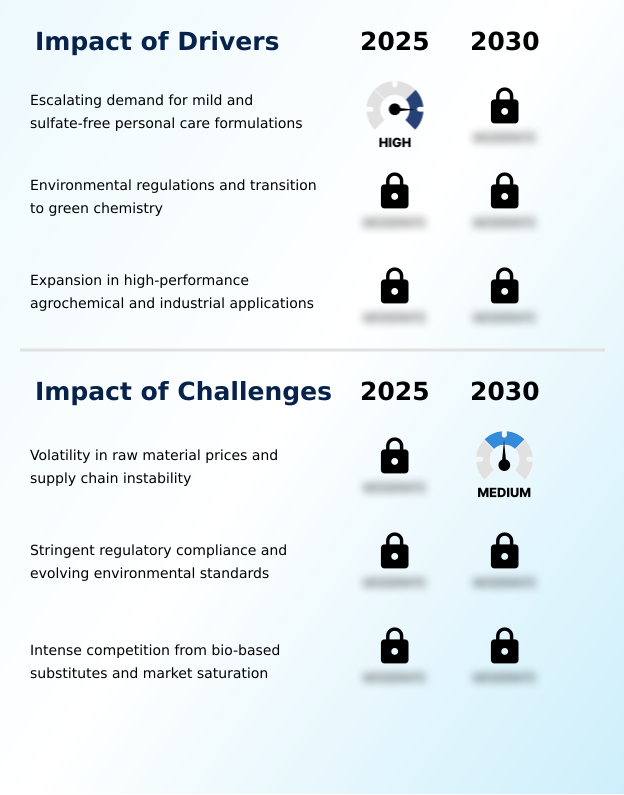

What are the key market drivers leading to the rise in the adoption of Amphoteric Surfactant Industry?

- Escalating demand for mild and sulfate-free personal care formulations is a key driver propelling growth in the amphoteric surfactant market.

- The primary driver remains the escalating demand for sulfate-free cleansing systems, where the pH-dependent charge behavior of amphoterics is essential.

- Consumer advocacy for safety has cemented their role in personal care, while their superior hard water tolerance and hydrotropic properties expand their use in industrial cleaning surfactants.

- Formulators rely on advanced formulation science to achieve the right cost-performance ratio, with specialized technical support services becoming a key competitive differentiator.

- For example, firms offering application-specific innovation for agrochemical adjuvants or corrosion inhibitor chemistry can command a 10% price premium.

- This expansion into high-performance industrial verticals helps diversify revenue and reduces the industry's reliance on the personal care sector, contributing to a more balanced and resilient market structure focused on environmental footprint reduction.

What are the market trends shaping the Amphoteric Surfactant Industry?

- The market is experiencing a significant trend toward the acceleration of bio-based feedstocks. This shift is coupled with a growing emphasis on certified sustainability to meet evolving regulatory and consumer demands.

- A significant market trend is the acceleration of sustainable ingredient sourcing, driven by consumer demand for non-irritating formulations and products with a favorable biodegradable surfactant profile. This shift is compelling manufacturers to move away from petrochemical derivatives, despite challenges like vegetable oil price volatility, and toward green alternatives.

- The secondary surfactant function of amphoterics is crucial in creating advanced dermo-cosmetic ingredients. Innovations in cold-processable surfactants are improving manufacturing efficiency by over 10%. As regulatory compliance costs rise, the adoption of a digital product passport is becoming essential for supply chain resilience.

- This focus on sustainability is reshaping formulation science, with foam boosting agents and viscosity modification now expected to come from eco-friendly sources, leading to a 15% increase in the launch of certified bio-based products.

What challenges does the Amphoteric Surfactant Industry face during its growth?

- Volatility in raw material prices and ongoing supply chain instability present a key challenge to the amphoteric surfactant industry's growth trajectory.

- The market faces intense competition from next-generation rhamnolipid biosurfactants and sophorolipid alternatives produced via microbial fermentation surfactants. This is a core challenge for specialty chemical manufacturing, as these alternatives align with green chemistry principles and appeal to consumers seeking fully bio-based ingredients. Asset optimization strategy and nearshoring production trends are being explored to counter high manufacturing costs.

- The upstream chemical ecosystem is under pressure to deliver cost-competitive feedstocks for traditional amphoterics, such as oilfield demulsifiers and textile processing auxiliaries. Companies must create value-added formulations and innovate beyond standard food-grade emulsifiers to compete.

- The shift toward biosurfactants has already captured approximately 5% of the niche mild surfactant market, forcing traditional producers to pivot their strategies for downstream specialty chemicals.

Exclusive Technavio Analysis on Customer Landscape

The amphoteric surfactant market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the amphoteric surfactant market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Amphoteric Surfactant Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, amphoteric surfactant market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Alfa Chemistry - Delivering advanced formulation science through a portfolio of high-purity amphoterics and specialty chemical manufacturing, designed to enhance performance in dermo-cosmetic ingredients and value-added formulations.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Alfa Chemistry

- BASF SE

- Clariant International Ltd.

- Croda International Plc

- Dow Chemical Co.

- Elementis Plc

- Evonik Industries AG

- Galaxy Surfactants Ltd.

- Huntsman International LLC

- Kao Corp.

- Lonza Group Ltd.

- Nouryon Chemicals Holding B.V.

- PCC SE

- Stepan Co.

- The Lubrizol Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Amphoteric surfactant market

- In August 2024, Galaxy Surfactants launched a new zwitterionic surfactant engineered to meet consumer demand for safe, sustainable ingredients in home and personal care products.

- In November 2024, Indorama Ventures, through its Indovinya segment, announced an agreement to acquire the KEMELIX and FLOWSOLVE brands from Cargill Bioindustrial, strengthening its specialty surfactants portfolio for the energy sector.

- In March 2025, Indonesia announced plans to raise its palm oil export levy, a move impacting the global supply chain and cost structure for oleochemical-based surfactants.

- In April 2025, BASF launched Dehyton PK45 GA/RA, a cocamidopropyl betaine derived from Rainforest Alliance Certified coconut oil, offering formulators a high-performance ingredient with a verifiable sustainable supply chain.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Amphoteric Surfactant Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 308 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 7.1% |

| Market growth 2026-2030 | USD 1932.5 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 6.5% |

| Key countries | China, Japan, India, South Korea, Australia, Indonesia, Germany, UK, France, Italy, Spain, The Netherlands, US, Canada, Mexico, Brazil, Argentina, Colombia, Saudi Arabia, UAE, South Africa, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The market's evolution is anchored in advanced zwitterionic surfactant chemistry, which enables pH-dependent charge behavior and unique hydrotropic properties. The industry is pivoting from petrochemical derivatives toward sustainable oleochemical feedstocks for cocamidopropyl betaine synthesis and the creation of other high-purity amphoterics, including amine oxide surfactants and sultaine derivatives.

- This shift supports the development of non-irritating formulations with a favorable biodegradable surfactant profile, essential for dermo-cosmetic ingredients and sulfate-free cleansing systems. Key performance attributes such as secondary surfactant function, viscosity modification, and foam boosting agents are refined in low-salt surfactant systems.

- For boardroom strategy, the decision to invest in green chemistry principles and microbial fermentation surfactants like rhamnolipid biosurfactants or sophorolipid alternatives is critical for long-term competitiveness. Companies adopting these technologies have reported a 20% improvement in their renewable carbon index.

- This transition also impacts industrial applications, including agrochemical adjuvants, corrosion inhibitor chemistry, oilfield demulsifiers, food-grade emulsifiers, and textile processing auxiliaries, where hard water tolerance and cold-processable surfactants are valued.

- Adherence to EU Ecolabel compliance and mass balance certification, supported by robust REACH registration data and aquatic toxicity assessment, is now a baseline for market access, influencing the design of high-active formulations and concentrated detergent systems.

What are the Key Data Covered in this Amphoteric Surfactant Market Research and Growth Report?

-

What is the expected growth of the Amphoteric Surfactant Market between 2026 and 2030?

-

USD 1.93 billion, at a CAGR of 7.1%

-

-

What segmentation does the market report cover?

-

The report is segmented by Application (Personal care, Household cleaning, Agrochemicals, and Others), Type (Betaines, Aminoxides, and Others), End-user (Cosmetics, Food and beverage, and Others) and Geography (APAC, Europe, North America, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

APAC, Europe, North America, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Escalating demand for mild and sulfate-free personal care formulations, Volatility in raw material prices and supply chain instability

-

-

Who are the major players in the Amphoteric Surfactant Market?

-

Alfa Chemistry, BASF SE, Clariant International Ltd., Croda International Plc, Dow Chemical Co., Elementis Plc, Evonik Industries AG, Galaxy Surfactants Ltd., Huntsman International LLC, Kao Corp., Lonza Group Ltd., Nouryon Chemicals Holding B.V., PCC SE, Stepan Co. and The Lubrizol Corp.

-

Market Research Insights

- The market dynamics are shaped by a complex interplay of performance requirements and cost pressures. While the threat of rivalry is moderate, the push for sustainable ingredient sourcing is compelling manufacturers to innovate beyond commodity chemical pricing. Formulations leveraging advanced amphoterics can reduce reliance on secondary thickeners by up to 15%, enhancing cost-performance ratios.

- Although price sensitivity among buyers is high, the impact of quality on output is significant, with formulators prioritizing performance over incremental cost savings in over 70% of premium hair care ingredient applications. This focus on value-added formulations and dermo-cosmetic compatibility underscores a market where technical support services and application-specific innovation are key differentiators.

We can help! Our analysts can customize this amphoteric surfactant market research report to meet your requirements.