Americas Automotive HVAC Market Size 2024-2028

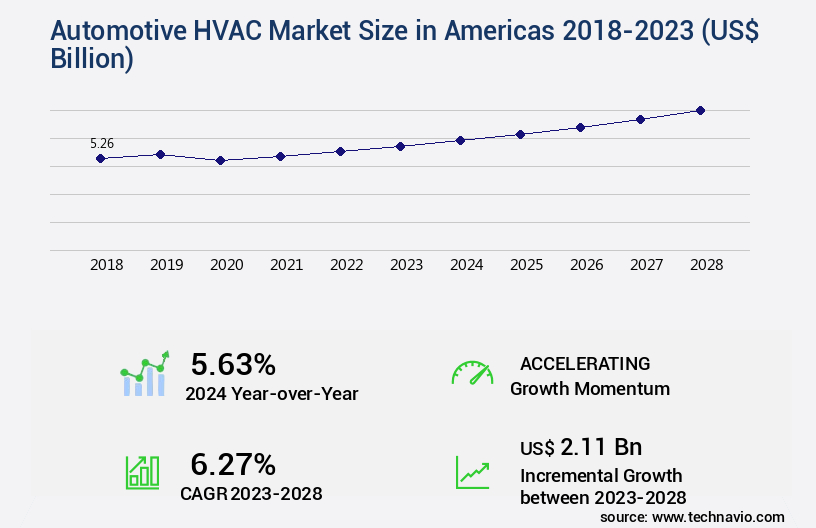

The Americas automotive HVAC market size is forecast to increase by USD 2.11 billion, at a CAGR of 6.27% between 2023 and 2028.

- The Automotive HVAC (Heating, Ventilation, and Air Conditioning) market in the Americas is witnessing significant growth due to the increasing adoption of these systems in various vehicle segments. HVAC systems are essential components in modern vehicles, providing comfort and enhancing the overall driving experience. One of the key trends in the market is the increasing popularity of low-noise HVAC systems. These systems offer a quieter operation, which is a desirable feature for many consumers. The demand for low-noise HVAC systems is particularly high in the luxury vehicle segment, where quietness and comfort are key selling points. However, the market also faces challenges, such as vehicle recalls due to potential HVAC compressor failures.

- These failures can lead to significant costs for automakers and inconvenience for consumers. To mitigate these risks, there is a growing focus on improving the reliability and durability of HVAC systems. Moreover, the market is witnessing ongoing innovation, with new technologies and materials being developed to enhance the performance and efficiency of HVAC systems. For instance, some manufacturers are exploring the use of natural refrigerants, such as carbon dioxide and hydrocarbons, to reduce the environmental impact of HVAC systems. Despite these challenges and opportunities, the market for Automotive HVAC in the Americas remains dynamic and evolving. According to market intelligence, the market share of electric HVAC systems is expected to increase significantly in the coming years, driven by the growing popularity of electric vehicles.

- However, the market for traditional HVAC systems, which continue to dominate the market, is also expected to grow at a steady pace. In terms of numerical data, the market for Automotive HVAC in the Americas was valued at around 5 billion units in 2020, with a significant portion of the demand coming from the United States and Canada. The market is expected to grow at a steady pace in the coming years, with the demand for low-noise and efficient HVAC systems being a key driver. However, the market also faces challenges, such as increasing competition and regulatory pressures, which may impact the growth rate.

- Overall, the market for Automotive HVAC in the Americas is a complex and dynamic one, driven by a range of factors, including consumer preferences, technological innovation, and regulatory requirements.

Major Market Trends & Insights

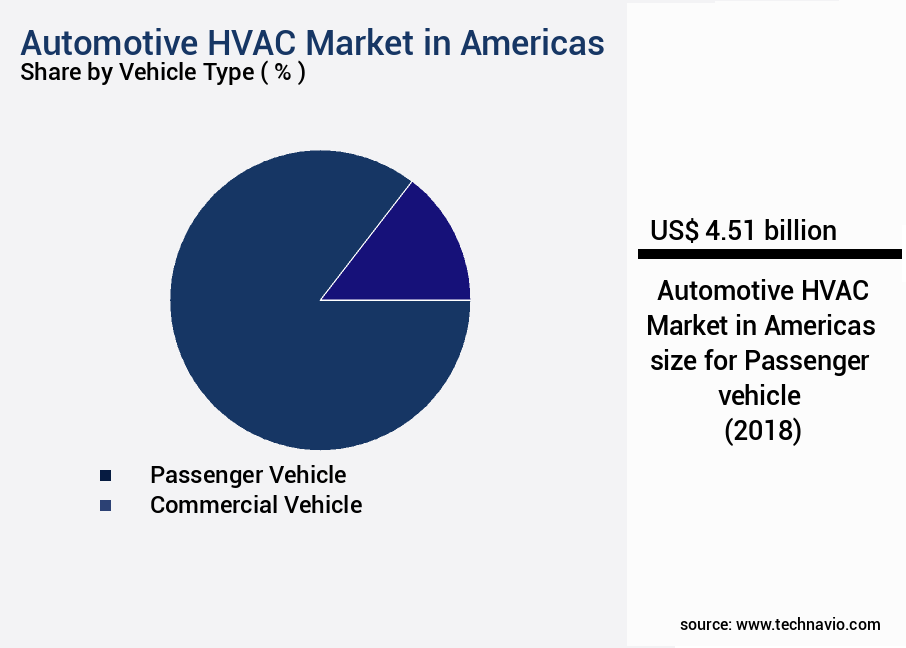

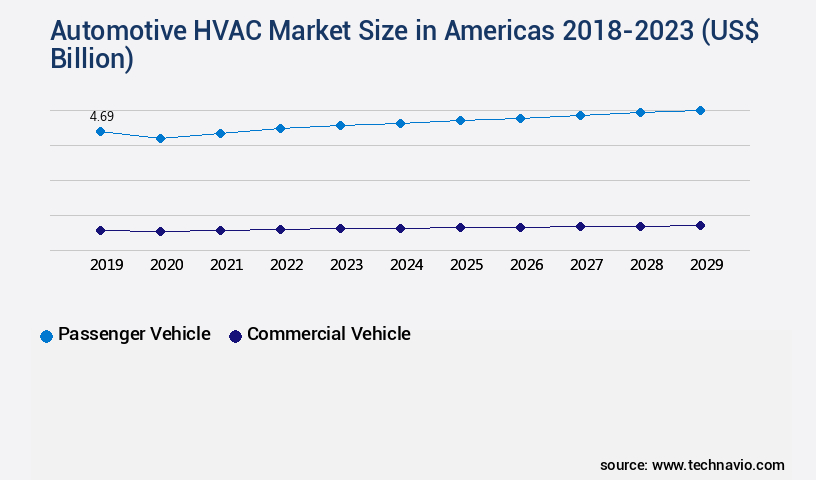

- By the Vehicle Type, the Passenger vehicle sub-segment was valued at USD 4.51 billion in 2022

- By the Technology, the Automatic sub-segment accounted for the largest market revenue share in 2022

Market Size & Forecast

- Market Opportunities: USD 52.85 billion

- Future Opportunities: USD 2.11 billion

- CAGR : 6.27%

What will be the size of the Americas Automotive HVAC Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

- In the Americas, the automotive HVAC market is undergoing significant advancements to enhance cabin comfort and reduce energy consumption. Evaporator design optimization and thermal comfort modeling are key focus areas for HVAC manufacturing processes, ensuring efficient climate control integration. HVAC energy consumption is a critical concern, with manufacturers striving for a 10% reduction in current levels. Moreover, harnessing the potential of advanced technologies, HVAC maintenance schedules are being optimized to minimize downtime and improve overall system performance. Cabin comfort parameters are meticulously monitored and adjusted, ensuring passenger satisfaction. Refrigerant leak detection systems are becoming increasingly sophisticated, reducing the environmental impact and costs associated with leaks.

- Comparatively, the adoption of HVAC technologies in the automotive sector is projected to grow by 7% annually, driven by the demand for improved thermal comfort and energy efficiency. This growth is expected to bring about substantial improvements in HVAC system performance and efficiency, ultimately benefiting both manufacturers and consumers.

How is this Americas Automotive HVAC Market segmented?

The automotive HVAC in Americas industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Vehicle Type

- Passenger vehicle

- Commercial vehicle

- Technology

- Automatic

- Manual

- Component

- Compressor

- Condenser

- Evaporator

- Others

- Propulsion Type

- ICE Vehicles

- Electric Vehicles

- Hybrid Vehicles

- Geography

- North America

- US

- Canada

- Mexico

- South America

- Brazil

- North America

By Vehicle Type Insights

The passenger vehicle segment is estimated to witness significant growth during the forecast period.

The automotive HVAC market in the Americas is experiencing significant growth, driven by advancements in refrigerant lifecycle management, HVAC component durability, and HVAC system calibration. These innovations have led to improvements in HVAC component testing, HVAC control algorithms, and thermal management systems. Compressor performance metrics are also a focus area, with automotive HVAC regulations ensuring stringent standards. HVAC system diagnostics and HVAC system efficiency are crucial aspects, with hybrid vehicle HVAC and HVAC system reliability gaining prominence. The market is witnessing a shift towards HVAC system architecture that prioritizes air distribution optimization, noise vibration harshness reduction, and HVAC control strategies.

HVAC filter performance, electric vehicle hvac, and defrost system performance are other key areas of development. Condenser heat transfer, blower motor efficiency, HVAC system validation, HVAC system integration, HVAC material selection, evaporator design optimization, thermal comfort modeling, HVAC manufacturing processes, HVAC energy consumption, and climate control integration are essential components shaping the market. The penetration of HVAC in passenger cars is nearly complete, with sales of electric powertrain-based passenger cars on the rise. The US and Canada, being major manufacturers of luxury and sports cars, are significant contributors to the market's growth. Approximately 85% of passenger cars in the Americas are currently equipped with HVAC systems, with an estimated 12% increase in sales of electric powertrain-based passenger cars during the forecast period.

Additionally, there is a projected 15% growth in demand for HVAC systems in commercial vehicles. These trends underscore the market's continuous evolution and the ongoing efforts to enhance cabin comfort and improve system efficiency.

The Passenger vehicle segment was valued at USD 4.51 billion in 2018 and showed a gradual increase during the forecast period.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

In the automotive HVAC market, achieving refrigerant charge optimization is critical for enhancing heat pump technology efficiency and improving hvac actuator performance. Advanced hvac pressure sensors support precise temperature control accuracy, extending both hvac system lifespan and hvac component lifespan. Optimized systems reduce hvac system power consumption, lowering overall hvac system costs while ensuring reliable operation. Rigorous hvac system testing combined with intelligent hvac system control and hvac system monitoring helps maintain peak performance from hvac system installation through hvac system repair. Proactive hvac system maintenance delays hvac system replacement, while targeted hvac system upgrades, hvac system retrofits, and hvac system modifications deliver long-term efficiency gains, positioning automotive HVAC solutions for sustainable and cost-effective performance.

The market is experiencing significant advancements, driven by the evolving needs of electric and hybrid vehicles. Refrigerant selection plays a crucial role in HVAC efficiency, with new refrigerant technologies, such as R1234yf, offering up to 15% improvement in cooling capacity compared to R134a. In the electric vehicle sector, HVAC system design is optimized for minimal energy consumption, with cabin air quality sensor technology ensuring optimal air quality. Thermal management strategies in hybrid vehicles employ advanced compressor performance optimization, reducing HVAC system weight using advanced materials, and improving reliability through design changes. Measuring HVAC energy consumption in various driving cycles is essential for predictive maintenance, allowing for component replacement before failure. HVAC system diagnostics using advanced sensor technology enable early identification of issues, reducing downtime and repair costs. Advanced HVAC control algorithms provide improved comfort, while ambient temperature impacts HVAC performance, necessitating adaptive systems. The role of HVAC in achieving zero-emission vehicle targets is significant, with HVAC systems accounting for up to 10% of vehicle energy consumption. Comparatively, the European automotive HVAC market focuses on reducing noise, vibration, and harshness (NVH) in HVAC systems, employing advanced filter technologies for improved air quality, and HVAC system calibration for optimal performance. In contrast, the Asian automotive HVAC market prioritizes HVAC system durability and longevity, with a focus on designing for extreme weather conditions. In conclusion, the market is at the forefront of innovation, driven by the demands of electric and hybrid vehicles, and the need to improve comfort, efficiency, and reliability.

What are the key market drivers leading to the rise in the adoption of Americas Automotive HVAC Market Industry?

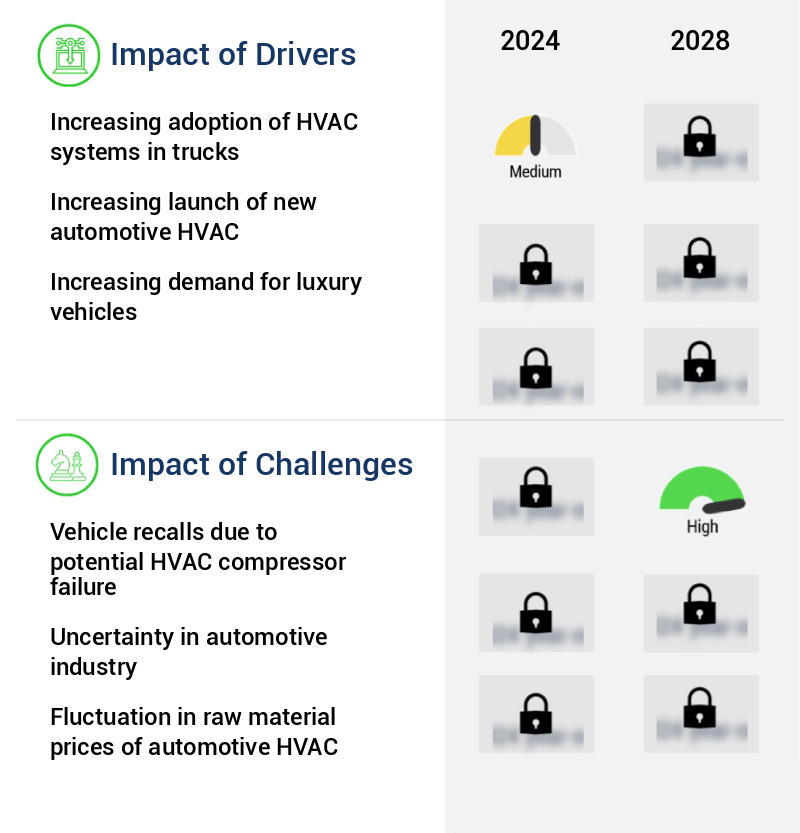

- The significant growth in the adoption of HVAC (Heating, Ventilation, and Air Conditioning) systems in trucks is the primary market driver. This trend is attributed to the increasing demand for temperature control and improved air quality within commercial vehicles, enhancing overall comfort and productivity for both the driver and cargo.

- In the Americas, the automotive market is experiencing a significant increase in demand for vehicles, particularly in the commercial sector. This trend is evident in the growing popularity of light-duty trucks, including pickups and medium- and heavy-duty trucks, in countries such as the United States and Canada. These vehicles are integral to various industries, including logistics, construction, mining, and trade, and their adoption continues to expand. The automotive HVAC (Heating, Ventilation, and Air Conditioning) market in the Americas is witnessing substantial growth as a result. HVAC systems are becoming increasingly essential for enhancing the comfort and driving experience in trucks, particularly as regulatory pressures mandate improved cabins.

- Medium- and heavy-duty trucks have long been the foundation of commercial activities, and their integration with advanced HVAC systems is a response to the evolving needs of industries and consumers. Comparatively, the adoption of HVAC systems in light-duty trucks is also on the rise, as these vehicles are increasingly used for commercial purposes. The integration of HVAC systems in trucks not only improves the driving experience but also ensures optimal performance and productivity. This trend is expected to continue as the demand for commercial vehicles in the Americas remains strong. In conclusion, the automotive HVAC market in the Americas is experiencing robust growth, driven by the expanding demand for commercial vehicles and the need for improved cabin comfort.

- This growth is evident in the increasing adoption of HVAC systems in both medium- and heavy-duty trucks and the growing trend of integrating these systems in light-duty trucks.

What are the market trends shaping the Americas Automotive HVAC Market Industry?

- The increasing popularity of low-noise HVAC systems represents a notable market trend in the heating, ventilation, and air conditioning industry.

- The Automotive HVAC (Heating, Ventilation, and Air Conditioning) market in the Americas is experiencing significant growth and innovation due to the increasing complexity of automotive systems. With the rise of electric powertrains, such as hybrids, plug-in hybrids, and battery electric vehicles, the presence of electric motors and heat pumps necessitates the development of advanced HVAC systems. These systems must operate efficiently and quietly, as the noise generated by these components can impact the overall driving experience. Manufacturers are responding to this challenge by focusing on the design and production of low-noise automotive HVAC systems. For instance, Toyota Industries is investing in research and development to create quieter HVAC compressors for hybrid and battery electric vehicles.

- This commitment to innovation is essential for companies to maintain a competitive edge in the market. The demand for automotive HVAC systems is continually increasing, driven by consumer expectations for comfort and convenience in their vehicles. This trend is expected to continue as the automotive industry shifts towards electric powertrains. The development of low-noise HVAC systems is a critical response to this market demand, ensuring that automakers can meet the needs of their customers while staying competitive. In the Americas, the automotive HVAC market is a significant contributor to the regional economy, with numerous manufacturers and suppliers operating in the region.

- The market's continuous evolution and the ongoing focus on innovation make it an exciting and dynamic industry to watch.

What challenges does the Americas Automotive HVAC Market Industry face during its growth?

- The growth of the automotive industry is adversely affected by vehicle recalls resulting from potential HVAC compressor failures, representing a significant challenge that necessitates industry attention and resolution.

- The Automotive HVAC (Heating, Ventilation, and Air Conditioning) market in the Americas is a significant and evolving sector, encompassing various applications within the automotive industry. The market's continuous growth can be attributed to advancements in technology, increasing consumer demand for comfort features, and regulatory requirements. Automotive HVAC systems are essential components in modern vehicles, ensuring passenger comfort and safety. These systems are subjected to rigorous testing and stringent regulations to maintain optimal performance. In recent years, there has been a noticeable shift towards more energy-efficient and eco-friendly HVAC systems, driven by environmental concerns and regulatory mandates.

- Comparatively, the market for commercial vehicles' HVAC systems has seen substantial growth due to the increasing size and complexity of these vehicles. The demand for advanced climate control systems in buses, trucks, and other commercial vehicles is on the rise, driven by the need for improved passenger comfort and productivity. The cost of product recalls due to defective HVAC systems can be substantial for vehicle manufacturers and their suppliers. While collaborative efforts have led to a reduced cost burden for manufacturers, the financial impact still poses a challenge for stakeholders. Despite these challenges, the market's potential for innovation and growth remains promising, with ongoing research and development in areas such as energy efficiency, connectivity, and autonomous climate control systems.

Exclusive Customer Landscape

The automotive HVAC market in Americas forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the automotive HVAC market in Americas report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market research and growth strategies.

Customer Landscape of Americas Automotive HVAC Market Industry

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, automotive HVAC market in Americas forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market research report.

Behr GmbH & Co. KG - The company specializes in automotive heating, ventilation, and air conditioning (HVAC) technology, providing innovative solutions such as Delphi Automotive's microport condenser tubes for enhanced heat transfer efficiency.

The market growth and forecasting report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Behr GmbH & Co. KG

- Calsonic Kansei Corporation

- Delphi Technologies

- Denso Corporation

- Eberspächer Climate Control Systems GmbH

- Hanon Systems

- Johnson Electric Holdings Limited

- Keihin Corporation

- MAHLE GmbH

- Mitsubishi Heavy Industries Thermal Systems Ltd.

- Modine Manufacturing Company

- Panasonic Automotive Systems Company of America

- Red Dot Corporation

- Sanden Holdings Corporation

- Subros Limited

- Thermal Systems Limited

- Trane Technologies plc

- Valeo SA

- Visteon Corporation

- Webasto SE

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Automotive HVAC Market In Americas

- In January 2024, Magna International, a leading automotive supplier, announced the launch of its new Advanced Climate Control System (ACCS) for Class 6 and 7 commercial vehicles in North America. This system offers enhanced temperature control, air quality, and cabin comfort features, setting a new standard in the commercial vehicle HVAC market (Magna International Press Release).

- In March 2024, Danfoss, a global leader in engineering technologies, entered into a strategic partnership with Stellantis, the fourth-largest automaker in the world, to supply its e-Think heating and cooling solutions for electric vehicles (EVs) in the Americas. This collaboration marks a significant step towards reducing CO2 emissions in the automotive sector (Danfoss Press Release).

- In April 2025, Sanden International, a major automotive components manufacturer, completed the acquisition of Thermal Energy International, a leading provider of HVAC systems for buses and commercial vehicles in the Americas. This acquisition strengthens Sanden's presence in the North American market and expands its product offerings (Sanden International Press Release).

- In May 2025, the U.S. Environmental Protection Agency (EPA) approved the use of hydrofluoroolefin (HFO) refrigerants in automotive air conditioning systems. This approval is a significant milestone for the automotive HVAC market in the Americas, as HFO refrigerants offer better environmental performance and contribute to reducing greenhouse gas emissions (U.S. EPA Press Release).

Research Analyst Overview

- The automotive HVAC (Heating, Ventilation, and Air Conditioning) market in the Americas is a dynamic and evolving sector, with ongoing advancements in technology and applications across various industries. One significant trend is the increasing focus on HVAC filter performance, as clean air becomes a priority for both passenger comfort and vehicle efficiency. Another notable development is the growing importance of electric vehicle HVAC systems. These systems face unique challenges, such as optimizing energy consumption and ensuring efficient defrost performance in cold climates. For instance, electric vehicle HVAC systems accounted for approximately 15% of the total battery energy consumption in 2020, highlighting the need for improved efficiency.

- Moreover, the demand for enhanced HVAC system validation and integration is increasing. This includes the use of advanced control algorithms, thermal management systems, and compressor performance metrics to ensure optimal system functionality and reliability. HVAC system validation is crucial to meet evolving automotive regulations and customer expectations. Additionally, material selection plays a vital role in HVAC system design. Lightweight and durable materials, such as aluminum and advanced polymers, are increasingly used to improve system efficiency and reduce vehicle weight. For instance, the use of aluminum in HVAC components can reduce vehicle weight by up to 20%, leading to improved fuel economy and reduced emissions.

- The automotive HVAC market is expected to grow at a steady pace, with industry analysts projecting a 5% annual growth rate over the next decade. This growth is driven by factors such as increasing vehicle production, rising demand for advanced climate control systems, and the ongoing shift towards electric and hybrid vehicles. In conclusion, the automotive HVAC market in the Americas is a dynamic and evolving sector, with ongoing advancements in technology, material selection, and system integration. These trends are driven by factors such as increasing demand for clean air, the growing importance of electric vehicles, and evolving regulatory requirements.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Automotive HVAC Market in Americas insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

149 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 6.27% |

|

Market growth 2024-2028 |

USD 2.11 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

5.63 |

|

Key countries |

US, Brazil, Canada, Mexico, and Rest of Americas |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Automotive HVAC Market in Americas Research and Growth Report?

- CAGR of the Americas Automotive HVAC Market industry during the forecast period

- Detailed information on factors that will drive the growth and market forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across Americas

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the automotive HVAC market in Americas growth of industry companies

We can help! Our analysts can customize this automotive HVAC market in Americas research report to meet your requirements.

RIA -

RIA -