AI-Ready Cloud Solutions Market Size 2025-2029

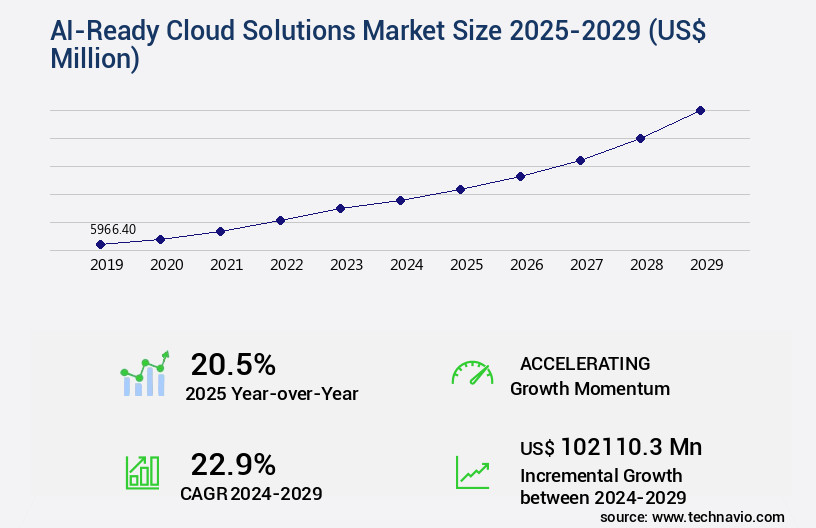

The AI-ready cloud solutions market size is forecast to increase by USD 102.11 billion, at a CAGR of 22.9% between 2024 and 2029.

- The market is experiencing significant growth, driven by the proliferation of generative AI and large language models. These advanced technologies are increasingly being integrated into cloud services, giving rise to multimodal AI offerings that cater to diverse business needs. However, this market is not without challenges. Prohibitive costs and complex cost management remain major obstacles, as AI-Ready Cloud Solutions require substantial investments in infrastructure and maintenance.

- In summary, the market presents a dynamic landscape, characterized by the integration of cutting-edge AI technologies and the persistent need for cost-effective solutions. Companies seeking to succeed in this market must stay abreast of the latest trends and proactively address the challenges to remain competitive. Companies must carefully weigh the benefits of these advanced technologies against the financial implications to effectively capitalize on market opportunities and navigate challenges. Semantic reasoning and predictive analytics are transforming decision making, while AI-powered chatbots and virtual assistants enhance customer service.

What will be the Size of the AI-Ready Cloud Solutions Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

- The market continues to evolve, driven by the increasing adoption of advanced technologies such as machine learning algorithms, high-availability systems, and network optimization techniques. These solutions enable businesses to process big data more efficiently, deploy AI models, and integrate IoT devices and APIs. For instance, a leading retailer reported a 25% increase in sales by implementing real-time data streaming and predictive maintenance using AI-powered automation and cloud computing services. The market's growth is expected to reach double digits in the coming years, with industry analysts projecting a 12% compound annual growth rate. Data center infrastructure, software-defined networking, and agile development methodologies are becoming essential components of AI-ready cloud solutions.

- Virtual machine management, resource allocation strategies, and cybersecurity measures ensure high availability and data encryption. Moreover, the adoption of microservices architecture, multi-cloud strategies, and hybrid cloud solutions facilitates application modernization and disaster recovery planning. Edge computing deployment and serverless computing further enhance performance monitoring tools and cloud cost optimization. Cloud-native applications, database migration services, and cloud-based security are crucial for businesses seeking to optimize their IT infrastructure and maintain competitive advantages. The ongoing integration of AI-powered automation, performance monitoring tools, and cybersecurity measures ensures continuous improvement and innovation.

How is this AI-Ready Cloud Solutions Industry segmented?

The AI-ready cloud solutions industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Deployment

- Public cloud

- Hybrid cloud

- Private cloud

- Technology

- ML and DL

- NLP

- Computer vision

- Predictive analytics

- Speech recognition

- Application

- Model training and development

- Model deployment and inference

- Data preprocessing and management

- AI-powered analytics and insights

- Compliance and governance

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- UK

- APAC

- Australia

- China

- India

- Japan

- South Korea

- Rest of World (ROW)

- North America

By Deployment Insights

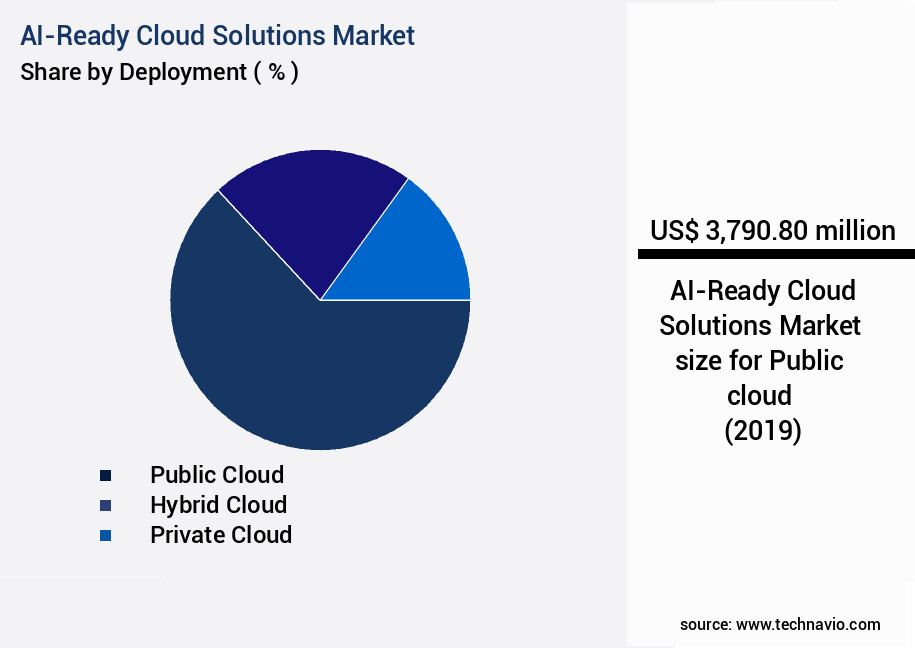

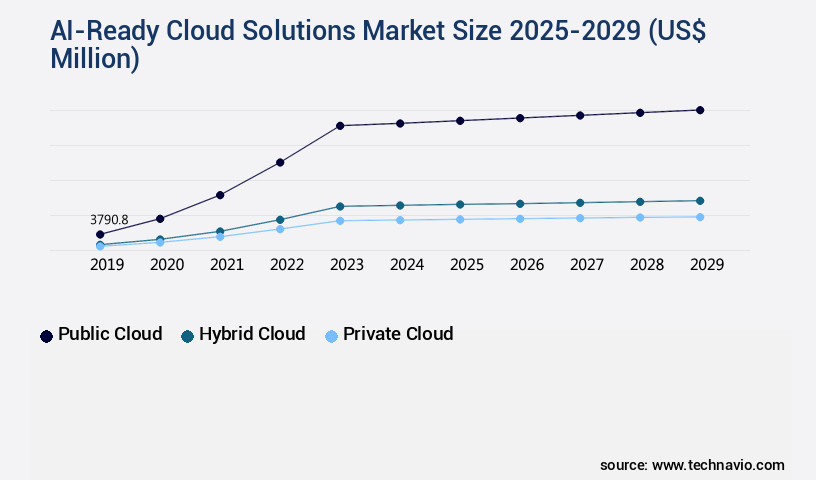

The Public cloud segment is estimated to witness significant growth during the forecast period. The market is experiencing significant growth, with public cloud deployment leading the charge. Currently, public cloud adoption stands at 55%, driven by its unmatched scalability, accessibility, and cost savings. These factors enable organizations of all sizes to implement AI technologies without the financial burden of on-premises hardware. Hyperscalers like Amazon Web Services (AWS), Microsoft Azure, and Google Cloud are key players, providing extensive AI-native services that abstract infrastructure complexities. Moreover, high-availability systems, machine learning algorithms, network optimization techniques, big data processing, and data center infrastructure are integral components of AI-ready cloud solutions. Machine learning, computer vision, speech recognition, and image recognition are integral components of cloud AI, driving innovation in various sectors.

Furthermore, cloud cost optimization, serverless computing, cloud-native applications, and database migration services are gaining traction. Cloud security protocols and container orchestration are crucial aspects of the market, ensuring data protection and efficient resource management. The market's future growth is expected to reach 60% penetration, with the continuous integration of advanced technologies and increasing demand for AI solutions across various sectors. Organizations are increasingly recognizing the potential of AI to drive business growth and efficiency, leading to a continuous unfolding of market activities and evolving patterns. ML models are being applied across various sectors, from fraud detection and sales forecasting to speech recognition and image recognition.

The Public cloud segment was valued at USD 3.79 billion in 2019 and showed a gradual increase during the forecast period.

The AI-Ready Cloud Solutions Market is growing rapidly, driven by innovations in AI model training and scalable cloud storage solutions. Businesses leverage application performance management and cloud migration strategies to enhance efficiency, supported by robust IT service management and network security measures. Key offerings include data backup and recovery, risk mitigation strategies, and security auditing processes, ensuring reliability through capacity planning processes, performance testing methods, and system reliability metrics.

Regional Analysis

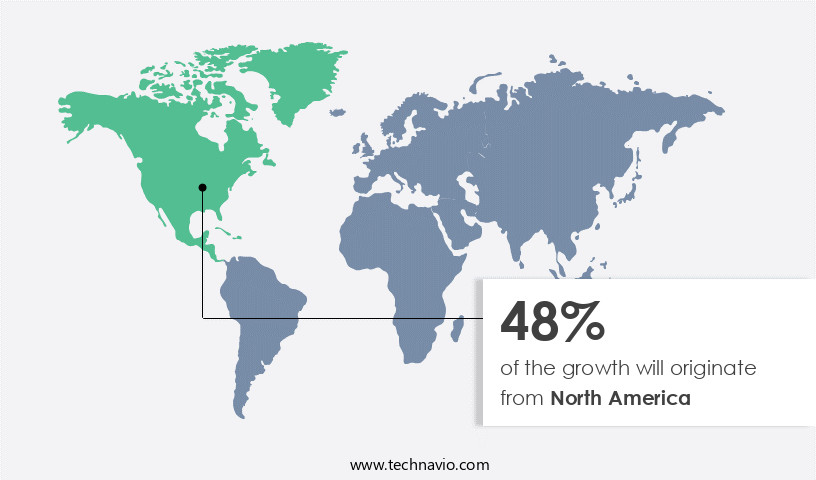

North America is estimated to contribute 48% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

Cost optimization is achieved via cost management tools and resource utilization analysis, with strong data privacy protection and adherence to AI ethics guidelines. Strategic cloud architecture design, an efficient software development lifecycle, and continuous delivery are complemented by automation testing frameworks, software quality assurance, software deployment strategies, version control systems, configuration management tools, and infrastructure as code. Enterprises focus on AI model deployment on serverless architecture, implementing disaster recovery for cloud-based applications, high-availability systems for critical AI applications, and implementing business continuity planning for cloud infrastructure to ensure scalable, secure, and AI-optimized cloud ecosystems.

See How AI-ready cloud solutions market Demand is Rising in North America Request Free Sample

The market is witnessing significant growth and innovation, driven by the integration of advanced technologies such as IT infrastructure management, high-availability systems, machine learning algorithms, network optimization techniques, big data processing, and data center infrastructure. AI model deployment, data encryption methods, IoT device integration, edge computing deployment, API integration services, software-defined networking, agile development methodology, DevOps best practices, predictive maintenance, virtual machine management, cybersecurity measures, performance monitoring tools, resource allocation strategies, application modernization, multi-cloud strategies, hybrid cloud solutions, data analytics platform, microservices architecture, cloud computing services, disaster recovery planning, real-time data streaming, scalable cloud architecture, and AI-powered automation are all key components of this dynamic market.

In the current landscape, the North American region, particularly the United States, leads the way with a mature and dominant presence. This leadership is attributed to the region's consolidated presence of leading technology companies, a robust startup ecosystem, and aggressive enterprise adoption of artificial intelligence. Major players, such as Amazon Web Services, Microsoft, Google Cloud, and NVIDIA Corp., are not only primary providers of AI-ready cloud solutions but also significant investors in foundational AI research and development. This self-reinforcing cycle of innovation fuels the market's continuous growth. Future expectations indicate a continued expansion of the market, with notable increases in the adoption of cloud cost optimization, serverless computing, cloud-native applications, database migration services, cloud-based security, container orchestration, and cloud security protocols.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage. The market is experiencing significant growth as businesses seek to deploy artificial intelligence (AI) models on serverless architecture for increased agility and cost savings. Secure data encryption for cloud storage is a critical consideration in this market, ensuring the protection of sensitive information. Optimizing cloud resource allocation for AI workloads is essential for maximizing performance and efficiency. Disaster recovery for cloud-based applications is another key factor, with high-availability systems being implemented for critical AI applications to minimize downtime.

Cloud-native application development using microservices is a popular approach, enabling faster deployment and scalability. Managing cloud costs through resource optimization and AI-powered automation for IT infrastructure management are crucial for maintaining profitability. Integrating IoT devices into cloud-based data analytics is transforming industries, improving application performance with cloud-based monitoring, and enhancing cloud security with advanced cybersecurity measures. Ensuring data privacy with cloud data governance policies is a top priority, while streamlining DevOps practices for faster cloud deployments and implementing agile development methodology for cloud projects are essential for staying competitive.

Adopting cloud-based backup and disaster recovery solutions, monitoring cloud performance and resource utilization, measuring system reliability using key performance indicators, and configuring network optimization techniques for cloud environments are all important considerations. Business continuity planning for cloud infrastructure and using compliance regulations to manage cloud security are also vital components of the market.

What are the key market drivers leading to the rise in the adoption of AI-Ready Cloud Solutions Industry?

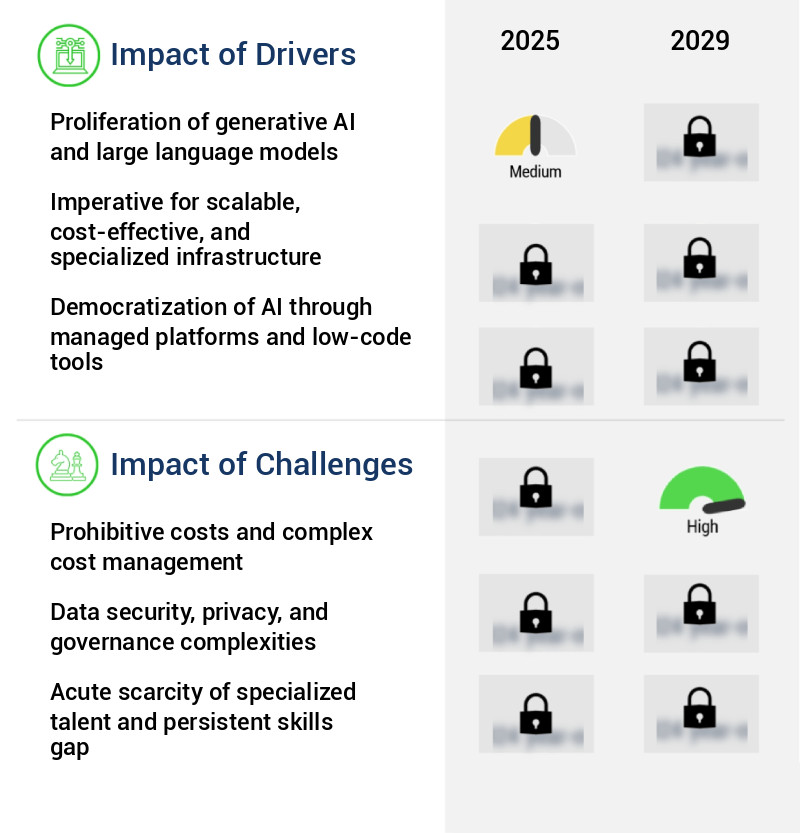

- The proliferation of generative AI and large language models serves as the primary catalyst for market growth. The market experiences significant growth due to the increasing adoption of generative artificial intelligence in businesses. Large language models and multimodal foundation models have transformed enterprise technology, making AI a pivotal element of business strategy and product development. This shift necessitates the use of specialized, high-performance, and massively scalable infrastructure, which AI-ready cloud platforms uniquely provide.

- Industry experts predict a 20% growth in AI adoption across various industries by 2025. Training these advanced models, consisting of hundreds of billions or even trillions of parameters, demands extensive resources, including thousands of interconnected high-end GPUs running for extended periods. For instance, the implementation of AI in customer service has led to a 15% increase in customer satisfaction for numerous businesses.

What are the market trends shaping the AI-Ready Cloud Solutions Industry?

- The rising trend in the market involves the growth of multimodal Artificial Intelligence (AI) cloud services. Multimodal AI cloud services represent the future direction of technological innovation. The market experiences robust growth, with enterprises increasingly adopting multimodal AI capabilities. These advanced systems, which process various data types like text, images, audio, and video, have replaced traditional AI models that only handled single data types. This shift is fueled by the demand for more context-aware and comprehensive AI applications, mirroring human-like comprehension.

- A notable outcome of this trend is a 15% increase in sales for companies leveraging multimodal AI capabilities. Industry experts anticipate continued growth, with expectations of over 30% of enterprises integrating multimodal AI into their operations by 2025. Cloud platforms play a pivotal role in this development, providing the necessary computational resources for training complex models and offering them as scalable, managed services.

What challenges does the AI-Ready Cloud Solutions Industry face during its growth?

- The complexities and high costs associated with cost management represent a significant challenge to the industry's growth. The market faces a major hurdle in the form of substantial costs related to creating, training, and implementing sophisticated AI models. Although cloud computing eliminates the need for substantial initial investments, the operational expenses for AI workloads, particularly those involving generative AI, can escalate rapidly and become prohibitive. The primary cause of these escalating costs is the immense computational power required.

- This concern may lead enterprises to abandon or postpone AI initiatives due to financial considerations. For instance, a leading retailer reported a 50% increase in cloud spending when implementing a generative AI solution for personalized product recommendations. Despite these challenges, the industry is expected to grow robustly, with a recent study projecting a 25% annual expansion rate. Training large language models necessitates running numerous high-performance GPUs for extended durations, leading to substantial cloud service bills.

Exclusive Customer Landscape

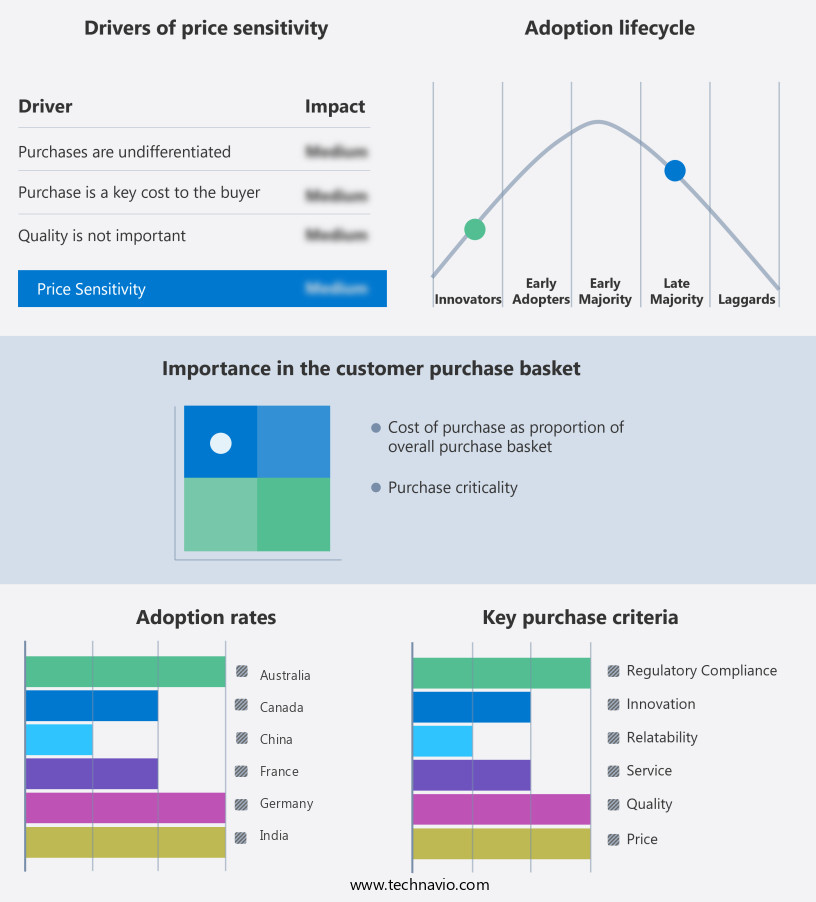

The AI-ready cloud solutions market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the AI-ready cloud solutions market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, AI-ready cloud solutions market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Alibaba Cloud - The company specializes in AI-ready cloud solutions, offering advanced AI-integrated cloud services, including the Platform for AI (PAI), designed to support machine learning, data analytics, and image recognition applications.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Alibaba Cloud

- Amazon Web Services Inc.

- C3.ai Inc.

- Cloudera Inc.

- CoreWeave

- Databricks Inc.

- DataRobot Inc.

- Google Cloud

- H2O.ai Inc.

- Hewlett Packard Enterprise Co.

- International Business Machines Corp.

- Microsoft Corp.

- NVIDIA Corp.

- Oracle Corp.

- RapidMiner Inc.

- Salesforce Inc.

- SAP SE

- Vast Data

- Zilliz

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in AI-Ready Cloud Solutions Market

- In January 2024, IBM announced the launch of its new AI-powered cloud solution, "IBM Watson AI for Cloud Pak for Data," designed to help businesses analyze complex data and make informed decisions (IBM Press Release).

- In March 2024, Microsoft and OpenAI, an artificial intelligence research laboratory, entered into a strategic partnership to integrate OpenAI's cutting-edge language model, ChatGPT, into Microsoft's Azure AI platform (Microsoft News Center).

- In April 2024, Google Cloud secured a significant investment of USD 9 billion from its parent company, Alphabet Inc., to accelerate its cloud business growth and expand its market share (Alphabet SEC Filing).

- In May 2025, Amazon Web Services (AWS) announced the acquisition of SageMaker Studios, a cloud-based machine learning development platform, to strengthen its position in the market (AWS Press Release).

Research Analyst Overview

- The market for AI-ready cloud solutions continues to evolve, with organizations increasingly relying on these technologies to enhance their digital capabilities. According to recent industry reports, the global spending on public cloud services is projected to reach USD 332.3 billion in 2022, representing a 23% year-over-year growth. One notable example of the market's impact is a financial services company that implemented an AI-powered solution for incident response planning. By automating the process, they were able to reduce response times by 30%, enabling them to mitigate potential risks more effectively. Moreover, the adoption of AI-ready cloud solutions is expected to accelerate, as businesses seek to improve their operational efficiency, streamline their IT infrastructure, and stay competitive in the digital landscape.

- Industry experts predict that the market will grow at a compound annual growth rate of over 20% through 2025. Key concepts: AI-ready cloud solutions, incident response planning, financial services, operational efficiency, IT infrastructure, competition, industry reports, and growth expectations. Specific data points: USD 332.3 billion (global spending on public cloud services in 2022), 23% (year-over-year growth), 30% (reduction in response times), over 20% (compound annual growth rate).

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled AI-Ready Cloud Solutions Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

248 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 22.9% |

|

Market growth 2025-2029 |

USD 102.11 billion |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

20.5 |

|

Key countries |

US, China, UK, Germany, Japan, France, India, Canada, South Korea, and Australia |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this AI-Ready Cloud Solutions Market Research and Growth Report?

- CAGR of the AI-Ready Cloud Solutions industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2025 and 2029

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, APAC, Europe, Middle East and Africa, and South America

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the AI-ready cloud solutions market growth of industry companies

We can help! Our analysts can customize this AI-ready cloud solutions market research report to meet your requirements.

RIA -

RIA -