AI In Cloud Contact Center Solutions Market Size 2025-2029

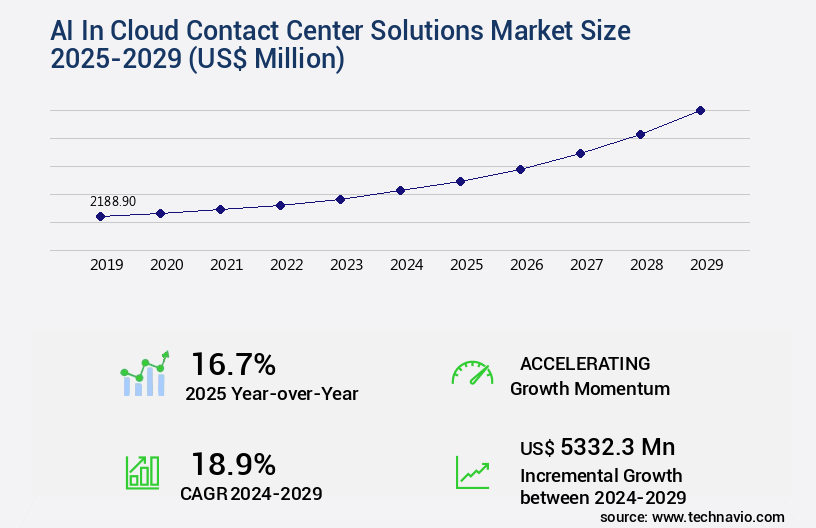

The ai in cloud contact center solutions market size is valued to increase by USD 5.33 billion, at a CAGR of 18.9% from 2024 to 2029. Escalating demand for hyper-personalized and omnichannel customer experiences will drive the ai in cloud contact center solutions market.

Major Market Trends & Insights

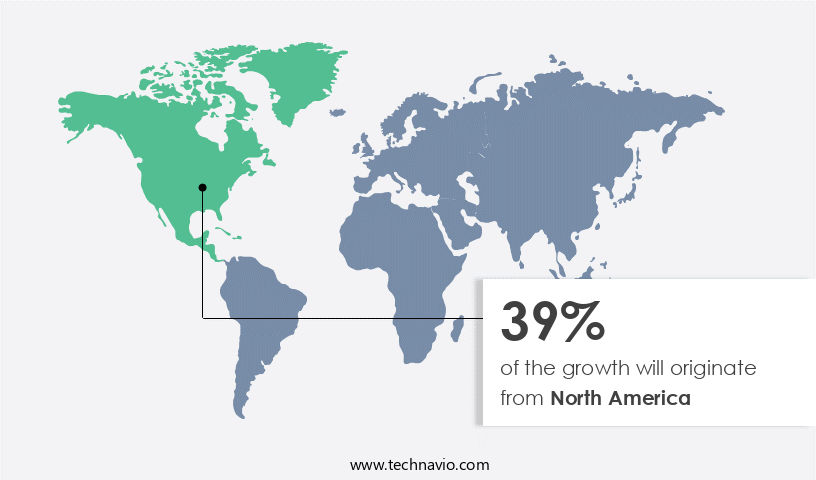

- North America dominated the market and accounted for a 39% growth during the forecast period.

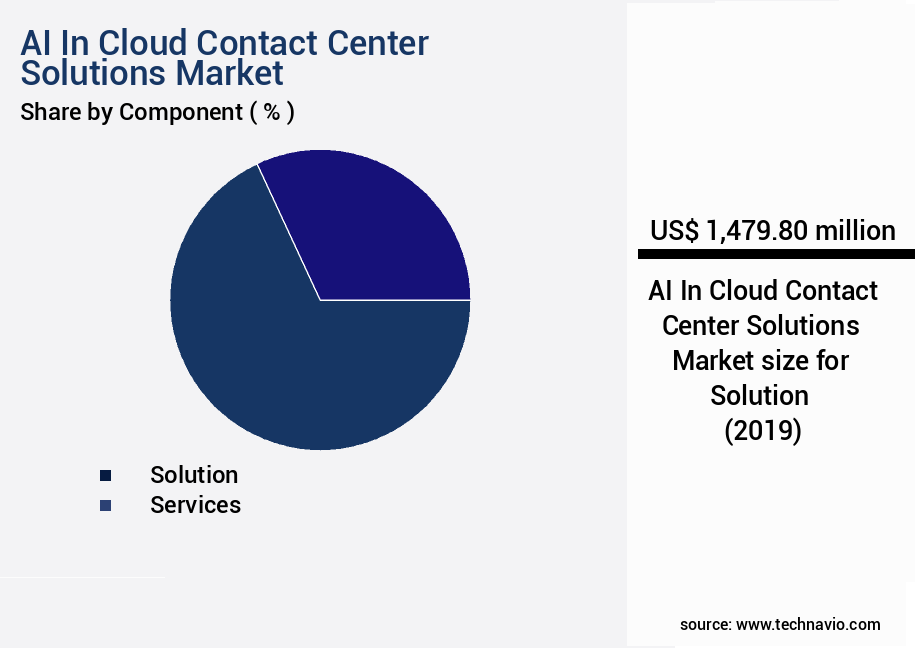

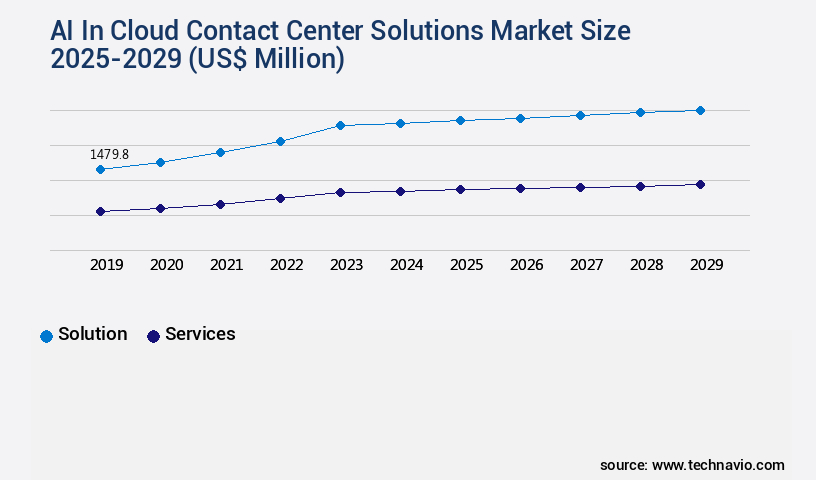

- By Component - Solution segment was valued at USD 1.48 billion in 2023

- By Application - Predictive call routing segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 321.06 million

- Market Future Opportunities: USD 5332.30 million

- CAGR from 2024 to 2029 : 18.9%

Market Summary

- In the dynamic business landscape, AI-infused cloud contact center solutions have emerged as a game-changer, revolutionizing customer engagement strategies. According to recent market intelligence, The market is projected to reach a value of USD3.9 billion by 2026, underscoring its significant growth potential. This surge in demand is driven by the escalating need for hyper-personalized and omnichannel customer experiences. Generative AI, a subset of artificial intelligence, plays a pivotal role in delivering personalized interactions at scale, enabling businesses to cater to diverse customer preferences and expectations.

- However, this technological evolution is not without challenges. Navigating complex data security, privacy, and regulatory compliance issues remains a significant hurdle. Despite these challenges, AI-driven cloud contact center solutions continue to gain traction, offering businesses the opportunity to streamline operations, enhance customer satisfaction, and drive growth in an increasingly competitive market.

What will be the Size of the AI In Cloud Contact Center Solutions Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the AI In Cloud Contact Center Solutions Market Segmented ?

The ai in cloud contact center solutions industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Component

- Solution

- Services

- Application

- Predictive call routing

- Workforce optimization

- Sentiment analysis

- Journey orchestration

- Others

- End-user

- BFSI

- Retail and e-commerce

- IT and telecom

- Healthcare and life science

- Others

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- UK

- APAC

- Australia

- China

- India

- Japan

- South Korea

- Rest of World (ROW)

- North America

By Component Insights

The solution segment is estimated to witness significant growth during the forecast period.

The market continues to evolve, with a growing emphasis on advanced technologies that enhance agent performance and optimize customer interactions. These solutions encompass a range of applications and platforms, from intelligent routing engines and machine learning models to dialogue management systems and natural language processing. One key development is the use of AI algorithms to replace traditional call routing systems, enabling predictive routing based on customer data, interaction history, and intent for improved first call resolution and customer satisfaction. Additionally, AI-powered chatbots and self-service options are becoming increasingly common, integrating with multi-channel platforms and utilizing natural language processing, sentiment analysis tools, and predictive analytics engines for a seamless customer journey.

With a scalable architecture design, these solutions offer real-time transcription, intent recognition, and quality monitoring systems, as well as API integrations and cloud-based infrastructure for enhanced security and flexibility. A recent study reveals that AI-driven contact centers have achieved an average handling time reduction of up to 25%, underscoring the significant impact of these technologies on operational efficiency and customer experience.

The Solution segment was valued at USD 1.48 billion in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 39% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How AI In Cloud Contact Center Solutions Market Demand is Rising in North America Request Free Sample

The North American market for AI in cloud contact center solutions is the most advanced and rapidly evolving segment globally. This region, comprising the United States and Canada, leads in the adoption of cutting-edge technologies, with businesses prioritizing customer experience in a highly competitive landscape. Key applications include AI-powered automation, agent augmentation, and self-service solutions. The primary growth drivers are the pursuit of operational efficiency and personalized customer engagement. High labor costs associated with traditional contact center operations serve as a significant catalyst for businesses to invest in AI technologies.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The market is experiencing significant growth as businesses seek to enhance customer experience and operational efficiency. AI-powered self-service chatbot integration is a key trend, allowing customers to resolve queries independently and reducing the workload on agents. Scalability is another critical factor, with cloud contact center platforms enabling businesses to easily expand their operations as they grow. Real-time sentiment analysis dashboards provide valuable insights into customer emotions, enabling agents to respond appropriately and improve customer satisfaction scores. Omnichannel routing efficiency metrics ensure that queries are directed to the most appropriate agent, reducing wait times and improving first call resolution.

Agent assist technology implementation, including predictive analytics for call routing and interactive voice response system design, empowers agents with the information they need to handle queries effectively. Contact center workforce optimization strategies, such as speech recognition accuracy improvement and natural language processing in chatbots, ensure that agents are equipped to handle complex queries and provide excellent customer service. AI-driven customer journey mapping enables businesses to gain a deeper understanding of their customers' needs and preferences, leading to more personalized interactions. Voice biometrics security enhancement and API integration with CRM systems ensure data security protocols are in place, while multi-channel integration strategies allow businesses to provide seamless customer experiences across all channels. Contact center analytics dashboards feature real-time transcription accuracy and agent performance monitoring systems, enabling businesses to identify trends and optimize their operations. Contact center automation workflows streamline processes and reduce costs, while ensuring that human agents are focused on providing high-value interactions. Overall, the adoption of AI in cloud contact center solutions is transforming the way businesses interact with their customers, leading to improved customer satisfaction and operational efficiency.

What are the key market drivers leading to the rise in the adoption of AI In Cloud Contact Center Solutions Industry?

- The escalating demand for hyper-personalized and omnichannel customer experiences is the primary market driver, as businesses strive to meet the increasing expectations of consumers who desire tailored interactions across multiple channels.

- The market is experiencing significant growth due to the increasing demand for seamless, contextual, and personalized customer interactions across multiple channels. Modern consumers expect brands to deliver a cohesive omnichannel journey, which traditional, on-premises contact center infrastructure struggles to provide efficiently. Cloud-native platforms, enhanced by AI, are becoming the preferred choice for businesses seeking to meet these evolving customer expectations. According to recent studies, the cloud contact center market is projected to reach a value of over USD20 billion by 2026, growing at a steady pace.

- Another report suggests that AI in contact centers is expected to save businesses over USD1 billion annually by streamlining operations and improving customer satisfaction.

What are the market trends shaping the AI In Cloud Contact Center Solutions Industry?

- The use of hyper-personalization at scale, facilitated by generative AI, is an emerging market trend. Generative AI technology enables the customization of experiences on a large scale, making hyper-personalization an increasingly significant market trend.

- The market is experiencing a transformative shift, with the integration of generative AI to deliver hyper-personalized customer experiences at an unprecedented scale. This evolution signifies a notable departure from traditional personalization methods, which relied on static rule sets and limited customer segmentation. Advanced Large Language Models (LLMs) are now enabling contact centers to generate dynamic, individualized interactions in real time, spanning all communication channels, including voice and digital messaging.

- This fundamental alteration of customer service and engagement is rooted in generative AI's capacity to comprehend context, discern intent, and produce human-like responses customized to each customer and their unique journey. This trend underscores the market's growing sophistication and adaptability to evolving customer needs.

What challenges does the AI In Cloud Contact Center Solutions Industry face during its growth?

- Ensuring data security, privacy, and adherence to intricate regulatory compliance are essential tasks that significantly impact the industry's growth trajectory.

- AI's integration into cloud contact centers has brought about new complexities, primarily concerning data security and privacy. Contact centers handle vast amounts of sensitive customer data, such as personally identifiable information (PII), financial details, and protected health information (PHI). The adoption of AI models, often managed by external providers, introduces potential risks for data breaches and misuse. Enterprises are increasingly vigilant about how customer data is utilized for AI training, its storage locations, and access control. A breach of this confidential data can result in substantial financial consequences, irreparable reputational damage, and a devastating loss of customer trust. This surge in adoption underscores the importance of robust data security measures and regulatory compliance in the realm of AI-powered contact center solutions.

Exclusive Technavio Analysis on Customer Landscape

The ai in cloud contact center solutions market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the ai in cloud contact center solutions market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of AI In Cloud Contact Center Solutions Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, ai in cloud contact center solutions market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Amazon Web Services Inc. - The company specializes in artificial intelligence integration for cloud contact center solutions, enhancing customer experiences through real-time transcription analysis with Amazon Connect and Contact Lens, conversational AI with Amazon Lex, and text-to-speech capabilities with Amazon Polly.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Amazon Web Services Inc.

- Cisco Systems Inc.

- Cresta

- Five9 Inc.

- Freshworks Inc.

- Genesys Telecommunications Laboratories Inc.

- Google Cloud

- Liveperson Inc.

- Microsoft Corp.

- NICE Ltd.

- Oracle Corp.

- Salesforce Inc.

- SAP SE

- Talkdesk Inc.

- UiPath Inc.

- Verint Systems Inc.

- Zendesk Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in AI In Cloud Contact Center Solutions Market

- In January 2024, Microsoft Corporation announced the integration of its AI-powered customer service solution, Microsoft Customer Service Insights, into its Microsoft Teams platform (Microsoft Press Release, 2024). This move aimed to streamline customer interactions and enhance the overall user experience.

- In March 2024, Amazon Web Services (AWS) and Genesys, a leading cloud contact center solutions provider, announced a strategic partnership to offer Genesys Cloud solutions on AWS Outposts (AWS Press Release, 2024). This collaboration enabled businesses to run Genesys workloads on-premises while leveraging AWS services, providing greater flexibility and control.

- In May 2024, NICE Limited, a global leader in customer experience solutions, acquired Inveritas, a contact center analytics company, for approximately USD135 million (NICE Press Release, 2024). This acquisition aimed to strengthen NICE's analytics capabilities and expand its offerings in the AI-driven contact center market.

- In April 2025, Google Cloud and Twilio announced a partnership to integrate Twilio's contact center solutions with Google Cloud's AI and machine learning capabilities (Google Cloud Blog, 2025). This collaboration aimed to provide businesses with advanced AI-driven contact center solutions, enabling more efficient and effective customer interactions.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled AI In Cloud Contact Center Solutions Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

248 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 18.9% |

|

Market growth 2025-2029 |

USD 5332.3 million |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

16.7 |

|

Key countries |

US, China, UK, Germany, Canada, Japan, France, India, South Korea, and Australia |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The market continues to evolve, with new applications and advancements emerging across various sectors. Agent performance metrics are enhanced through call routing optimization using machine learning models, ensuring customer satisfaction scores remain high. Dialogue management systems, integrated with natural language processing, facilitate efficient agent scheduling algorithms. Multi-channel integration, including self-service chatbots and interactive voice response, offers a seamless customer journey. Predictive analytics engines and sentiment analysis tools provide valuable insights, while real-time transcription and intent recognition engines streamline processes. Scalable architecture designs accommodate growth, with voice biometrics systems and text analytics capabilities ensuring data security.

- AI-powered chatbots and agent assist technology handle routine inquiries, freeing up agents for more complex tasks. Omnichannel routing and first call resolution improve customer experience. According to recent industry reports, the market is expected to grow by over 20% annually. For instance, a leading retailer implemented an AI-driven contact center solution, resulting in a 30% increase in first call resolution and a 25% reduction in average handling time.

What are the Key Data Covered in this AI In Cloud Contact Center Solutions Market Research and Growth Report?

-

What is the expected growth of the AI In Cloud Contact Center Solutions Market between 2025 and 2029?

-

USD 5.33 billion, at a CAGR of 18.9%

-

-

What segmentation does the market report cover?

-

The report is segmented by Component (Solution and Services), Application (Predictive call routing, Workforce optimization, Sentiment analysis, Journey orchestration, and Others), End-user (BFSI, Retail and e-commerce, IT and telecom, Healthcare and life science, and Others), and Geography (North America, APAC, Europe, Middle East and Africa, and South America)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, Middle East and Africa, and South America

-

-

What are the key growth drivers and market challenges?

-

Escalating demand for hyper-personalized and omnichannel customer experiences, Navigating data security, privacy, and complex regulatory compliance

-

-

Who are the major players in the AI In Cloud Contact Center Solutions Market?

-

Amazon Web Services Inc., Cisco Systems Inc., Cresta, Five9 Inc., Freshworks Inc., Genesys Telecommunications Laboratories Inc., Google Cloud, Liveperson Inc., Microsoft Corp., NICE Ltd., Oracle Corp., Salesforce Inc., SAP SE, Talkdesk Inc., UiPath Inc., Verint Systems Inc., and Zendesk Inc.

-

Market Research Insights

- The market for AI in cloud contact center solutions continues to evolve, integrating cognitive services to automate various functions and enhance customer interactions. Contact center automation, such as text-to-speech synthesis and speech-to-text conversion, improves efficiency and reduces labor costs. Real-time reporting systems and system uptime monitoring ensure high performance and reliability. Industry growth is expected to reach over 25% annually, driven by the increasing demand for proactive customer engagement and cost optimization strategies. For instance, a leading company in the sector reported a 30% increase in sales due to AI-powered agent training modules and empowerment tools.

- These solutions enable agents to handle more complex queries, improving overall service level agreements and customer satisfaction. Additionally, AI technologies like conversation AI, customer journey analytics, and workflow optimization techniques contribute to data privacy measures and compliance regulations.

We can help! Our analysts can customize this ai in cloud contact center solutions market research report to meet your requirements.

RIA -

RIA -