Agricultural Tractor Machinery Market Size 2025-2029

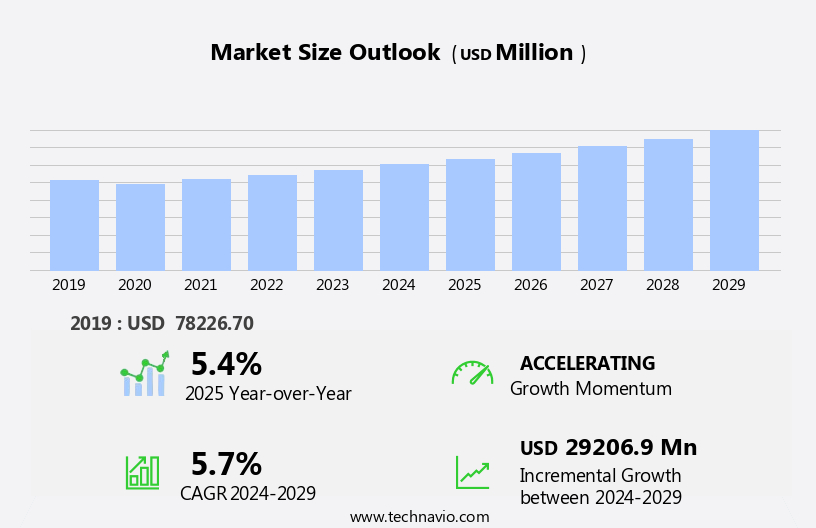

The agricultural tractor machinery market size is forecast to increase by USD 29.21 billion, at a CAGR of 5.7% between 2024 and 2029.

- The market is experiencing significant growth due to the increasing availability of machinery through rental options. This trend is particularly prominent in developing economies where farmers may not have the financial resources to purchase new equipment outright. Additionally, the integration of Artificial Intelligence (AI) in agricultural machinery is revolutionizing farming practices, enabling more efficient and precise farming operations. However, high costs remain a challenge for many farmers, limiting the adoption of advanced machinery and technology. Producers seeking to capitalize on market opportunities should consider offering flexible rental options and investing in AI technology to differentiate their offerings.

- Meanwhile, addressing the issue of high costs through innovative financing solutions or subsidies could unlock significant growth potential in the market. Overall, the market is poised for continued expansion, driven by the demand for productivity enhancements and technological advancements. Companies must navigate the challenges of cost and competition to capture market share and maintain a competitive edge.

What will be the Size of the Agricultural Tractor Machinery Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2019-2023 and forecasts 2025-2029 - in the full report.

Request Free Sample

The market is characterized by its continuous evolution and dynamic nature. This sector encompasses a wide range of equipment, from power take-off (pto) systems and input management solutions to safety features, GPS guidance systems, hydraulic pumps, and various agricultural machinery. These components are intricately interconnected, forming the backbone of modern farming operations. Tractor engines, operator cabs, and harvesting equipment are essential elements, powering the agricultural process from seed planting to crop production. Irrigation systems, fueled by advancements in hydraulic pumps and transmission systems, enable sustainable agriculture in arid regions. Precision farming, fueled by data acquisition and analysis, has become increasingly prevalent, with GPS guidance systems and machine learning algorithms driving yield optimization.

Safety features, such as ground clearance and operator protection, have gained significant importance in the market. Livestock farming applications necessitate specialized tractor implements and fuel consumption considerations. Lease agreements and financing options offer farmers flexibility in managing their equipment investments. The integration of artificial intelligence (AI) and remote sensing technology has revolutionized agricultural practices, enabling real-time data monitoring and analysis. Soil tillage, engine cooling systems, and tractor tires have all benefited from these advancements, leading to improved efficiency and productivity. The agricultural machinery landscape is further shaped by emissions standards and parts supply considerations. Hydraulic systems, control systems, and seed drills are all subject to ongoing advancements, driving the market forward.

The future of agricultural technology lies in the convergence of sustainable practices, data-driven insights, and innovative machinery designs.

How is this Agricultural Tractor Machinery Industry segmented?

The agricultural tractor machinery industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Type

- Wheel tractor

- Crawler tractor

- Application

- Farm

- Landscape garden

- Others

- Variant

- Less than 40 HP

- 41 to 100 HP

- More than 100 HP

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- Italy

- UK

- APAC

- China

- India

- Japan

- South Korea

- Rest of World (ROW)

- North America

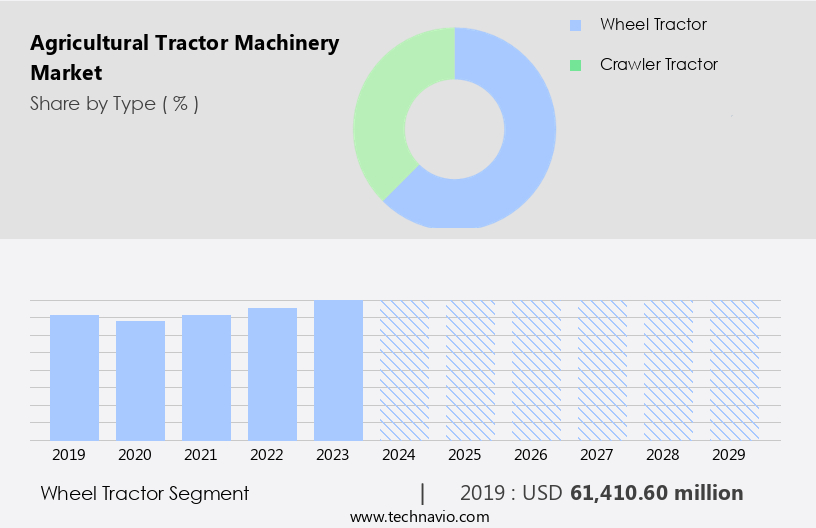

By Type Insights

The wheel tractor segment is estimated to witness significant growth during the forecast period.

The agricultural tractor market encompasses a range of machinery designed for farming operations, including harvesting equipment, irrigation systems, and tractor engines. Modern tractors are equipped with advanced technologies such as remote sensing, artificial intelligence, and machine learning, enhancing productivity and efficiency. Tractor implements like seed drills, plows, and cultivators are essential for crop production, while fuel efficiency, parts supply, and financing options are crucial considerations for farmers. Emissions standards and safety features are increasingly important in the tractor market, with a focus on sustainable agriculture and precision farming. Livestock farming also relies on tractors for tasks such as manure spreading and feeding operations.

Precision agriculture and data analytics enable farmers to optimize crop yields through real-time monitoring of fuel consumption, yield monitoring, and input management. Used tractors and transmission systems are popular choices for smaller farms or budget-conscious farmers. Hydraulic systems, engine cooling systems, and tractor tires are essential components that ensure the longevity and performance of agricultural tractors. Control systems, GPS guidance systems, hydraulic pumps, and agricultural machinery are integral to the efficient operation of modern farming equipment. In recent years, there has been a significant shift towards mechanized farming practices, with a focus on precision agriculture and sustainable farming techniques. This trend is driven by the need to increase productivity, reduce labor costs, and minimize the environmental impact of farming operations.

Agricultural technology continues to evolve, with innovations in soil tillage, irrigation systems, and tractor engines shaping the future of the agricultural sector.

The Wheel tractor segment was valued at USD 61.41 billion in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

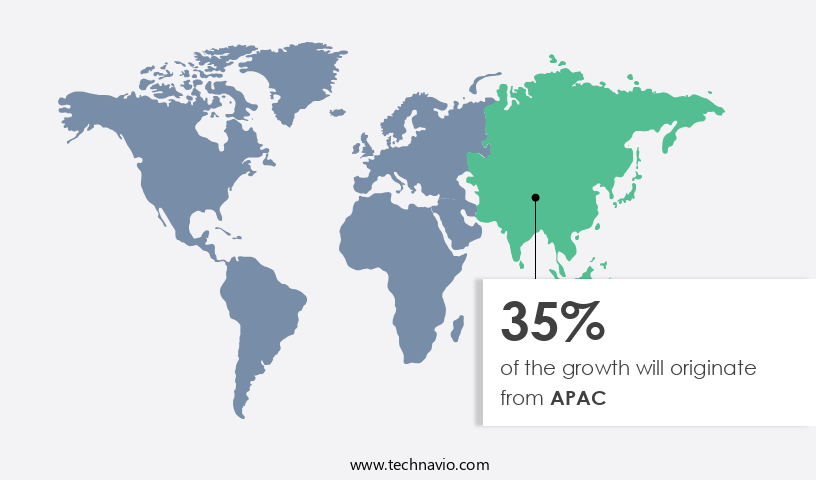

APAC is estimated to contribute 35% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

In the agricultural sector, the APAC region dominates the global tractor machinery market in 2024. Countries like China, India, Japan, Australia, and Indonesia are leading this trend due to their extensive agricultural industries. The transition from traditional farming methods to mechanized agriculture is crucial to increase efficiency and productivity, addressing the escalating food demand. Tractors play a significant role in this transformation, facilitating large-scale farming operations with tasks such as plowing, planting, harvesting, and transportation becoming more streamlined. Governments in APAC are promoting agricultural mechanization through various initiatives. Harvesting equipment, operator cabs, irrigation systems, and tractor engines are key components driving this market.

Advanced technologies like remote sensing, artificial intelligence (AI), and machine learning are integrated into agricultural machinery, enhancing precision farming and crop production. Fuel efficiency, parts supply, and emissions standards are essential considerations for tractor manufacturers. Financing options, drainage systems, seed drills, and precision agriculture are other significant market trends. Livestock farming and dairy farming also benefit from the use of agricultural tractors. Control systems, hydraulic systems, and transmission systems are integral to tractor functionality. Safety features, GPS guidance systems, hydraulic pumps, and data analytics are essential for modern farm equipment. Sustainable agriculture and soil tillage are growing areas of focus.

Engine cooling systems, tractor tires, and fuel consumption are essential factors for tractor performance. Lease agreements and power take-off (PTO) are essential for tractor implements. Input management and yield monitoring are critical for farmers to optimize their operations. Overall, the market is evolving to meet the demands of modern farming, integrating advanced technologies and focusing on efficiency and productivity.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The market is a dynamic and innovative sector, driven by advancements in technology and the growing demand for efficient farming solutions. This market encompasses a wide range of equipment, from compact tractors for small-scale farming to large, powerful models for industrial-scale agriculture. Key players in this market offer products featuring advanced features such as precision farming technology, automated guidance systems, and fuel efficiency. Additionally, the market is witnessing a trend towards electric and hybrid tractors, as sustainability becomes a top priority. Other significant trends include the integration of IoT and AI in tractor design, as well as the increasing popularity of multi-function tractors. Furthermore, the market is witnessing robust growth in emerging economies, particularly in Asia Pacific and Latin America, due to the rising agricultural sector in these regions. Overall, the market is a vibrant and evolving landscape, offering numerous opportunities for growth and innovation.

What are the key market drivers leading to the rise in the adoption of Agricultural Tractor Machinery Industry?

- The rental market for agricultural tractor machinery plays a crucial role in its expanding accessibility and growth, serving as a significant market driver.

- In the agricultural sector, the rental market for tractor machinery is experiencing significant growth due to the financial advantages it offers farmers. Renting enables farmers to access the latest technology and advanced features without the substantial upfront investment. Rental companies continuously update their inventory, ensuring farmers can utilize tractors with the most recent improvements. Moreover, the cost-effectiveness of renting is particularly beneficial for farmers with limited financial resources. Emissions standards are a crucial consideration in the agricultural machinery market. Farmers are increasingly adopting precision farming techniques, which require machinery with high data acquisition capabilities and ground clearance. Seed drills and transmission systems are essential components of precision agriculture, as they ensure accurate seed placement and efficient power transfer.

- Farmers also prioritize sustainability in their operations, leading to a growing interest in drainage systems that improve water management and reduce environmental impact. Used tractors remain a popular option due to their affordability, but farmers must ensure they meet emissions standards and undergo regular maintenance for optimal performance. In summary, the market is driven by the financial benefits of renting, the importance of meeting emissions standards, the adoption of precision farming, and the emphasis on sustainable agriculture. Renting allows farmers to access the latest technology, while precision farming and sustainability practices necessitate advanced machinery capabilities.

What are the market trends shaping the Agricultural Tractor Machinery Industry?

- The integration of artificial intelligence (AI) in agricultural machinery is an emerging market trend. This technological advancement is set to revolutionize the agricultural sector by enhancing efficiency, productivity, and precision in farming operations.

- Agricultural tractor machinery is undergoing significant advancements with the integration of agricultural technology. AI implementation is transforming farming practices by enabling autonomous tractor operation, reducing human intervention. Sensors, cameras, and GPS systems equip tractors to navigate fields, detect obstacles, and adjust paths. AI algorithms analyze collected data to optimize route planning, minimize overlap, and enhance field coverage. Precision farming techniques benefit from AI-powered tractors, as they apply inputs like fertilizers, pesticides, and water in a targeted and controlled manner. AI algorithms analyze soil sensor data, weather forecasts, and historical yield information to determine optimal input amounts and timings, minimizing waste and boosting crop health.

- Additionally, agricultural tractor machinery includes advanced engine cooling systems, tractor tires, and hydraulic systems for improved performance and fuel efficiency. Control systems ensure smooth operation and ease of use for livestock farming applications. Lease agreements provide farmers with flexible financing options for machinery acquisition. AI-driven agricultural technology continues to shape the future of farming, offering increased efficiency, productivity, and sustainability.

What challenges does the Agricultural Tractor Machinery Industry face during its growth?

- The escalating costs of agricultural machinery pose a significant challenge to the growth of the industry.

- Agricultural machinery manufacturing entails substantial research and development investments to create advanced equipment catering to farmers' specific requirements. The R&D process encompasses prototyping, testing, and refinement, leading to increased machinery prices due to these expenses. In the agricultural sector, machinery and equipment represent significant costs for farm businesses. The complexity of manufacturing advanced machinery and rising prices for larger machines, new technology, parts, and energy have contributed to the escalating costs. Advanced agricultural machinery integrates various features to enhance efficiency and productivity. Power take-off (PTO), hydraulic pumps, and hydraulic valves are essential components, while safety features, GPS guidance systems, and three-point hitches are vital for effective crop production.

- Data analytics plays a crucial role in optimizing farm operations and machinery utilization. Input management and efficient machinery operation are essential for farmers to maintain profitability and sustainability. Machinery manufacturers prioritize safety, efficiency, and precision in their designs, focusing on creating harmonious and immersive user experiences. The latest agricultural machinery incorporates advanced technology, emphasizing ease of use and minimal operator intervention. These innovations aim to streamline farm operations and improve overall productivity.

Exclusive Customer Landscape

The agricultural tractor machinery market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the agricultural tractor machinery market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, agricultural tractor machinery market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

AGCO Corp. - Agri-tech innovations power our large-scale farming machinery, maximizing productivity for global acreage enterprises through advanced technology and efficient design. Our offerings deliver unparalleled performance and sustainability in modern agriculture.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AGCO Corp.

- Alamo Group Inc.

- Argo Tractors SpA

- Caterpillar Inc.

- CLAAS KGaA mBH

- CNH Industrial NV

- Daedong Corp.

- Deccan Farm Equipments Pvt. Ltd.

- Deere and Co.

- ISEKI and Co. Ltd.

- JCB Co. Ltd.

- Jiangsu Yueda Intelligent Agricultural Equipment Co. Ltd.

- Kubota Corp.

- Mahindra and Mahindra Ltd.

- Mitsubishi Heavy Industries Ltd.

- SDF SpA

- Titan Machinery Inc.

- Tractors and Farm Equipment Ltd.

- Yanmar Holdings Co. Ltd.

- Zetor Tractors as

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Agricultural Tractor Machinery Market

- In January 2024, Deere & Company, a leading player in the market, announced the launch of its new X9 Series tractors. These high-performance tractors feature advanced technologies, including Auto-Guide 4000 precision agriculture system and IVT (Infinitely Variable Transmission), aiming to enhance farming efficiency and productivity (Deere & Company Press Release).

- In March 2024, AGCO Corporation and CNH Industrial N.V. Signed a memorandum of understanding to collaborate on the development of autonomous tractors and related technologies. This strategic partnership is expected to strengthen both companies' positions in the autonomous agricultural machinery market (CNH Industrial N.V. Press Release).

- In May 2024, Mahindra Tractor Limited secured a significant investment of INR 1,200 crores (approximately USD 156 million) from SBI CAP Fund, a subsidiary of State Bank of India. The investment will support Mahindra Tractor's expansion plans and product development initiatives (Mahindra Tractor Limited Press Release).

- In April 2025, John Deere received approval from the European Commission for its acquisition of Blue River Technology, a leading precision agriculture technology company. This acquisition is expected to strengthen John Deere's position in the precision agriculture market and provide advanced technologies for its agricultural machinery offerings (European Commission Press Release).

Research Analyst Overview

- The market is driven by the need for efficient and reliable equipment to support farming practices. Diesel engines continue to dominate the market due to their power and durability, while engine reliability remains a top priority for farmers. However, electric tractors are gaining traction, offering reduced emissions and lower operating costs. Fertilizer application and implement attachments are essential features, with warranty programs and servicing contracts ensuring equipment uptime. Automatic transmission, front-end loaders, and power shift transmission are popular transmission types, while manual transmission and CVT transmission cater to specific applications. Safety regulations and compliance standards shape the market, with a focus on operator training and safety features.

- Soil health, weed control, and pest control are critical farming techniques addressed by tractor accessories. Engine durability and technical support are essential for maintaining productivity, with hybrid tractors and alternative fuels, such as gasoline engines and biofuel engines, offering sustainability benefits. Farming practices continue to evolve, with water management and crop management systems optimizing resource usage. Training programs and rental services provide flexible solutions for farmers. Hydraulic components and transmission types, such as backhoe loaders and quick hitch systems, enhance tractor functionality. Harvest optimization and compliance with safety regulations are key considerations for farmers investing in new machinery.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Agricultural Tractor Machinery Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

205 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 5.7% |

|

Market growth 2025-2029 |

USD 29206.9 million |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

5.4 |

|

Key countries |

US, China, Japan, Germany, India, UK, South Korea, France, Canada, and Italy |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Agricultural Tractor Machinery Market Research and Growth Report?

- CAGR of the Agricultural Tractor Machinery industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2025 and 2029

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across APAC, Europe, North America, South America, and Middle East and Africa

- Thorough analysis of the market’s competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the agricultural tractor machinery market growth of industry companies

We can help! Our analysts can customize this agricultural tractor machinery market research report to meet your requirements.

RIA -

RIA -