Advertising Services Market Size 2025-2029

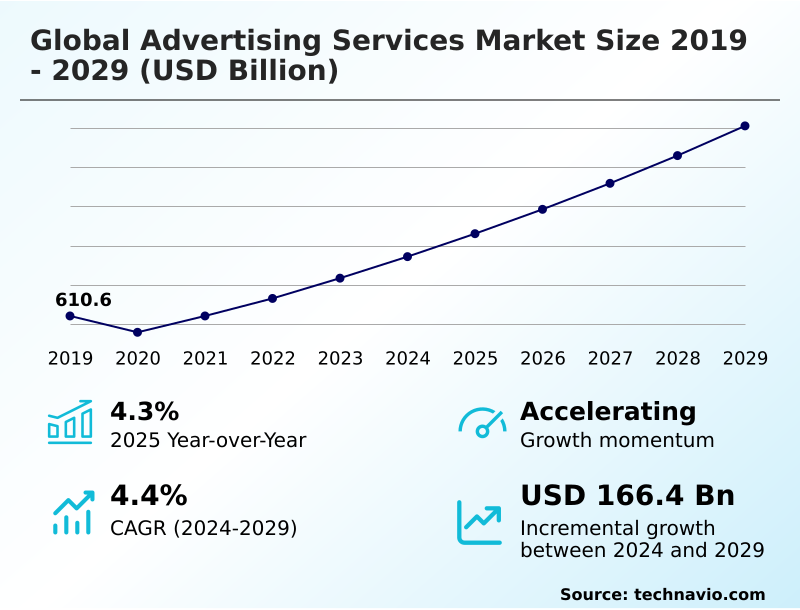

The advertising services market size is valued to increase by USD 166.4 billion, at a CAGR of 4.4% from 2024 to 2029. Accelerated digital transformation and ubiquity of connected devices will drive the advertising services market.

Major Market Trends & Insights

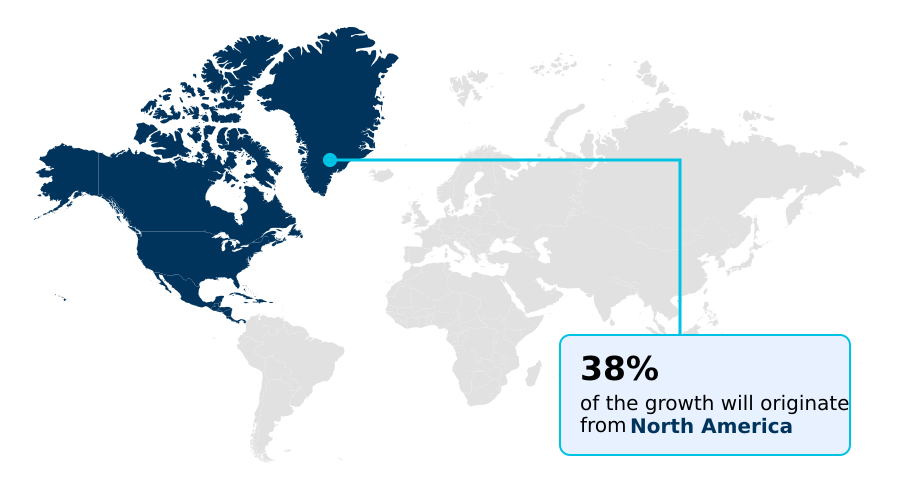

- North America dominated the market and accounted for a 38.4% growth during the forecast period.

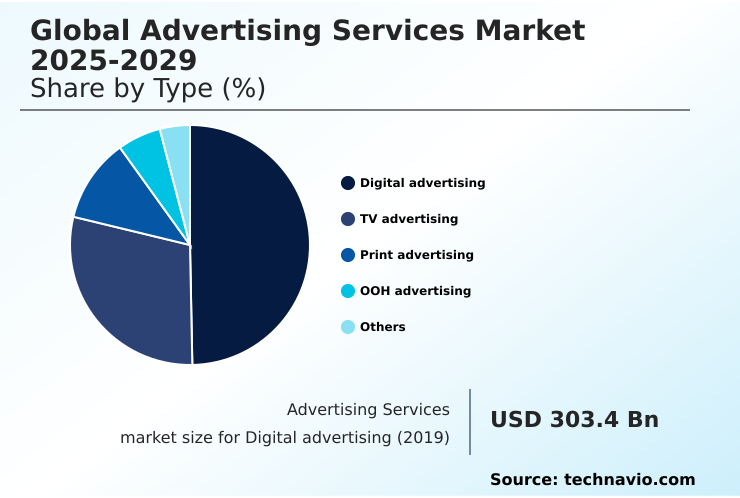

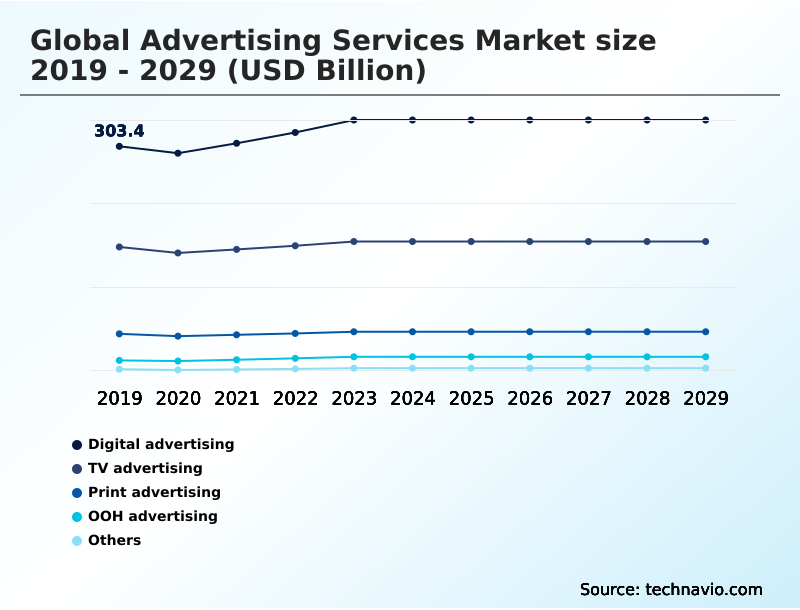

- By Type - Digital advertising segment was valued at USD 336.3 billion in 2023

- By Business Model - Online advertising segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 241.9 billion

- Market Future Opportunities: USD 166.4 billion

- CAGR from 2024 to 2029 : 4.4%

Market Summary

- The advertising services market is undergoing a significant transformation, driven by technological innovation and shifting consumer behaviors. The rise of retail media networks and the pervasive integration of generative AI are creating new efficiencies and channels for audience engagement. Organizations are leveraging these tools to automate creative production and deliver highly personalized campaigns at scale.

- However, this evolution is taking place against the backdrop of third-party cookie deprecation, which is forcing a fundamental industry shift toward privacy-enhancing technologies and first-party data strategies.

- A key business scenario involves consumer packaged goods companies using data clean rooms to collaborate with retailers, enriching their audience segmentation to launch more effective connected TV (CTV) campaigns without sharing personally identifiable information.

- This approach balances the demand for performance marketing and measurable return on ad spend with the critical need for user consent management and brand safety, defining the market's complex but opportunity-rich landscape.

What will be the Size of the Advertising Services Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Advertising Services Market Segmented?

The advertising services industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Type

- Digital advertising

- TV advertising

- Print advertising

- OOH advertising

- Others

- Business model

- Online advertising

- Offline advertising

- End-user

- Consumer goods and retail

- IT and telecom

- Government and public sector

- BFSI

- Others

- Geography

- North America

- US

- Canada

- Mexico

- APAC

- China

- India

- Japan

- Europe

- Germany

- UK

- France

- South America

- Brazil

- Argentina

- Colombia

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- North America

By Type Insights

The digital advertising segment is estimated to witness significant growth during the forecast period.

The digital advertising segment is evolving beyond simple metrics, focusing on comprehensive performance marketing strategies that integrate social commerce and shoppable video ads.

Success is increasingly measured not just by click-through rate (CTR) but by the overall return on ad spend (ROAS) and the efficacy of personalized ad delivery.

Advanced geotargeting technology is crucial for local engagement, while a sophisticated campaign flighting strategy optimizes budget allocation over time. The integration of programmatic advertising with first-party data activation enables precise digital ad trafficking and supports closed-loop attribution models.

This shift allows for a more holistic view of customer journeys, with firms using advanced attribution modeling seeing a 20% higher accuracy in crediting touchpoints.

The Digital advertising segment was valued at USD 336.3 billion in 2023 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 38.4% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Advertising Services Market Demand is Rising in North America Request Free Sample

The geographic landscape reveals divergent adoption rates for advanced advertising technologies. In North America and Europe, the focus is on optimizing real-time bidding (RTB) through sophisticated header bidding setups and the use of programmatic direct deals for premium inventory.

These mature markets are leading the charge in implementing universal ID solutions to navigate a cookieless future.

In contrast, high-growth markets in APAC and South America are seeing rapid expansion in mobile-first channels like in-game advertising and ad-supported video-on-demand (AVOD), with programmatic audio ads showing 40% higher engagement during commute times.

Across all regions, the supply-side platform (SSP) and ad exchange platforms are central to inventory management, while the effectiveness of contextual targeting is being re-evaluated as a privacy-safe alternative.

This disparity requires a globally-minded yet locally-tuned approach, with predictive audience modeling adapting to regional data signals and consumer behaviors on both subscription video-on-demand (SVOD) and free platforms.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Navigating the modern advertising ecosystem requires a sophisticated understanding of interconnected strategies. Key decisions revolve around measuring ROI in cookieless advertising and establishing best practices for generative AI creative. A critical evaluation is the retail media network vs programmatic debate, where brands weigh the benefits of closed-loop attribution against the scale of the open web.

- For video, implementing effective CTV advertising frequency capping strategies is essential to avoid audience fatigue. Strategically, implementing data clean rooms for partnerships is becoming a cornerstone for privacy-compliant data collaboration. Operationally, mitigating ad fraud in mobile apps and enabling brand safety controls for user-generated content are constant priorities.

- The core of modern strategy is building a first-party data strategy and optimizing campaigns with first-party data. This is supported by integrating CDP with a DSP and leveraging contextual targeting for privacy compliance. Using dynamic creative for personalized campaigns and effective attribution models for OOH are key tactics.

- The technical challenges include enabling cross-device targeting without cookies, creating commercially safe generative AI, and understanding the impact of signal loss on measurement. Firms that master a holistic approach, from leveraging AI for predictive audience buying to comparing universal ID solutions, see a more than 50% improvement in campaign efficiency.

- The focus extends to micro-optimizations like reducing ad load time for better UX and tactical decisions like audience verification in programmatic audio. Finally, developing strategies for walled garden advertising, using the privacy sandbox API for advertisers, and achieving full-funnel attribution for retail media are imperative for competitive advantage.

What are the key market drivers leading to the rise in the adoption of Advertising Services Industry?

- The accelerated pace of digital transformation, combined with the ubiquity of connected devices, is a key driver propelling market growth.

- Market growth is fueled by the strategic shift toward a first-party data strategy, enabled by the integration of a customer data platform (CDP).

- This allows for more precise journey orchestration ads and predictive audience modeling, which improves the effectiveness of automated media buying.

- The result is a more efficient media mix modeling process, where channels like addressable television advertising and augmented reality (AR) advertising can be measured more accurately.

- For example, location-based marketing, powered by this data, can increase foot traffic by up to 20%. The rise of influencer marketing platforms and affiliate marketing networks further diversifies reach, creating phygital experiences that bridge online and offline worlds.

- Advertisers are focused on optimizing cost per mille (CPM) through better targeting, with the ad server technology playing a crucial role in delivering these personalized messages.

What are the market trends shaping the Advertising Services Industry?

- The pervasive integration of generative artificial intelligence is emerging as a significant market trend, reshaping creative processes, campaign optimization, and audience personalization across the industry.

- Key trends are reshaping the advertising services market, led by the pervasive integration of generative AI and the proliferation of retail media networks. These networks, combined with the growth of connected TV (CTV) and ad-supported video-on-demand (AVOD), offer new avenues for audience segmentation.

- Advertisers utilize a demand-side platform (DSP) for efficient ad inventory management and to deploy dynamic creative optimization at scale. For instance, campaigns using AI-powered copywriting can achieve a 15% higher engagement rate. The creative landscape is also evolving, with anamorphic 3D billboards used in out-of-home (OOH) advertising to create immersive brand experiences.

- The fusion of content and commerce, or shoppertainment, is becoming mainstream, supported by native advertising formats that blend seamlessly with user experiences, driving both engagement and transactions.

What challenges does the Advertising Services Industry face during its growth?

- Navigating an increasingly stringent data privacy landscape and the imminent demise of third-party cookies presents a key challenge affecting industry growth.

- The market faces significant hurdles, primarily centered on third-party cookie deprecation and the need for robust brand safety protocols. This shift necessitates the adoption of cookieless identity solutions and privacy-enhancing technologies to maintain targeting capabilities. Navigating a walled garden ecosystem while ensuring ad verification remains a complex task.

- The industry's response includes the use of data clean rooms for secure data collaboration and a renewed focus on user consent management. For instance, implementing advanced ad fraud detection tools can reduce wasted spend by over 30%. Measurement is also evolving, with attention metrics gaining prominence over simple viewability metrics to gauge true engagement.

- Ensuring effective content-level targeting and server-side ad insertion without violating privacy is a key technical challenge, demanding sophisticated cross-channel measurement frameworks.

Exclusive Technavio Analysis on Customer Landscape

The advertising services market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the advertising services market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Advertising Services Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, advertising services market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Amazon.com Inc. - Provides solutions leveraging first-party shopper data, enabling brands to target consumers across e-commerce platforms and partner sites to enhance reach and sales impact.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Amazon.com Inc.

- Apple Inc.

- Criteo SA

- Dentsu Group Inc.

- Droga5

- Google Cloud

- Magnite Inc.

- Meta Platforms Inc.

- Microsoft Corp.

- Omnicom Group Inc.

- Pinterest Inc.

- Publicis Groupe SA

- PubMatic Inc.

- Reddit Inc.

- Snap Inc.

- The Interpublic Group of Companies Inc.

- The Trade Desk Inc.

- Wieden Kennedy

- WPP Plc

- X Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Advertising services market

- In October, 2024, Amazon.com Inc. announced a strategic partnership with Magnite Inc. to integrate its demand-side platform with Amazon's publisher services, expanding programmatic access to Amazon's ad inventory.

- In January, 2025, Publicis Groupe SA launched a proprietary generative AI platform, 'CreativeCore AI,' designed to automate campaign creative generation and performance analysis, reporting a 20% increase in creative asset production during trials.

- In March, 2025, The Trade Desk Inc. announced the full interoperability of its Unified ID 2.0 solution with several major European retail media networks, creating a standardized identity framework for advertising across the open internet.

- In May, 2025, WPP Plc announced a global strategic alliance with Microsoft Corp. to co-develop AI-powered advertising solutions on Microsoft's Azure cloud platform, aiming to provide clients with advanced audience modeling and campaign optimization tools.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Advertising Services Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 309 |

| Base year | 2024 |

| Historic period | 2019-2023 |

| Forecast period | 2025-2029 |

| Growth momentum & CAGR | Accelerate at a CAGR of 4.4% |

| Market growth 2025-2029 | USD 166.4 billion |

| Market structure | Fragmented |

| YoY growth 2024-2025(%) | 4.3% |

| Key countries | US, Canada, Mexico, China, India, Japan, South Korea, Australia, Indonesia, Germany, UK, France, Italy, The Netherlands, Spain, Brazil, Argentina, Colombia, Saudi Arabia, UAE, South Africa, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The advertising services market is fundamentally reshaped by the dual pressures of technological advancement and privacy-centric reforms. Boardroom decisions are now centered on the strategic implementation of a first-party data strategy, driven by the need to navigate third-party cookie deprecation.

- The pervasive integration of generative AI and dynamic creative optimization is not merely a tactical shift but a strategic imperative, forcing a re-evaluation of creative budgets and talent. Organizations leveraging these technologies have managed to reduce campaign production timelines by over 40%.

- The rise of retail media networks and connected TV (CTV) has fragmented the media landscape, demanding more sophisticated media mix modeling and attribution modeling. Consequently, technologies like the customer data platform (CDP), demand-side platform (DSP), and supply-side platform (SSP) are critical infrastructure.

- Executing campaigns via programmatic advertising, including programmatic direct and real-time bidding (RTB) on ad exchange platforms, is now standard.

- This complex environment, with its walled garden ecosystems, makes ad verification and ad fraud detection more critical than ever, with a constant focus on improving performance marketing metrics such as return on ad spend (ROAS) and click-through rate (CTR) while managing cost per mille (CPM).

What are the Key Data Covered in this Advertising Services Market Research and Growth Report?

-

What is the expected growth of the Advertising Services Market between 2025 and 2029?

-

USD 166.4 billion, at a CAGR of 4.4%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Digital advertising, TV advertising, Print advertising, OOH advertising, and Others), Business Model (Online advertising, and Offline advertising), End-user (Consumer goods and retail, IT and telecom, Government and public sector, BFSI, and Others) and Geography (North America, APAC, Europe, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Accelerated digital transformation and ubiquity of connected devices, Navigating increasingly stringent data privacy landscape and imminent demise of third party cookies

-

-

Who are the major players in the Advertising Services Market?

-

Amazon.com Inc., Apple Inc., Criteo SA, Dentsu Group Inc., Droga5, Google Cloud, Magnite Inc., Meta Platforms Inc., Microsoft Corp., Omnicom Group Inc., Pinterest Inc., Publicis Groupe SA, PubMatic Inc., Reddit Inc., Snap Inc., The Interpublic Group of Companies Inc., The Trade Desk Inc., Wieden Kennedy, WPP Plc and X Corp.

-

Market Research Insights

- The market's momentum is driven by the tension between technological advancement and privacy imperatives. The adoption of immersive brand experiences and shoppable video ads is creating more engaging consumer touchpoints, with early adopters reporting a 15% lift in user interaction.

- Concurrently, the need for robust privacy-enhancing technologies is non-negotiable, as platforms that implement transparent user consent management build greater consumer trust. Solutions offering closed-loop attribution are becoming standard, demonstrating up to a 30% clearer return on ad spend compared to traditional models.

- AI-powered copywriting and other forms of automation are streamlining workflows, enabling marketing teams to focus on strategy rather than repetitive execution. This dynamic interplay shapes a landscape where cross-channel measurement and efficiency are paramount.

We can help! Our analysts can customize this advertising services market research report to meet your requirements.

RIA -

RIA -